From app to platform: $DUOL enables personalized learning for everyone

Deep Dive — English Edition 🇬🇧/🇺🇸

FYI: This is the English translation of my Deep Dive in German. For the German version, please click here.

Many see Duolingo (ticker symbol: $DUOL) as just another language learning app. But it is actually much more than that: it is a platform that is just getting started and aims to redefine the global education market.

My analysis concludes that Duolingo is an extraordinary company and that the stock offers an asymmetric risk-reward ratio: high return potential with manageable risk. And that's not just because the stock has fallen 45% from its all-time high.

At first glance, the valuation of just under 12 times revenue combined with a market capitalization of $13 billion may seem high. However, it is clear that the stock market completely misunderstands the exceptional organizational characteristics of this company. And this gap between perception and reality creates a unique opportunity, which I will describe in more detail in the following sections.

Table of Contents

Reassessment of Duolingo stock on the horizon

Duolingo's success measurable by 4 key figures

Turning point thanks to new areas accelerated by AI

Competitive advantages in detail (7 Powers)

Analysis of the financial situation

Close-up look at the valuation of Duolingo shares

Risks due to high valuation, expansion, and AI

My conclusion

1) Reassessment of Duolingo stock on the horizon

On the surface, Duolingo may look like just another language learning app, but there is much more to it than that. In addition to language learning, Duolingo is introducing and expanding into other areas such as mathematics, music, and chess.

Duolingo is becoming a platform that enables personalized education for the mass market. Engagement on the platform is growing, and more and more users are becoming paying subscribers. At the same time, the cost of creating learning content is steadily declining thanks to a huge data advantage that is being leveraged by AI.

The company is at a fundamental turning point that will significantly boost revenues and profit margins.

2) Duolingo's success measurable by 4 key figures

If you take a closer look at these 4 metrics at Duolingo, you'll see that AI makes all areas of the company more efficient: from the creation of learning content to personalized AI tutors like Lily.

Increase in subscriber count

Higher revenue per subscriber

Improvement in cost structure

Increase in free cash flow per share

I. Increase in subscriber count

Duolingo's model is designed to convert free users into paying subscribers. Specifically, anyone with a smartphone and an internet connection can use the Duolingo app for free, but they have to tolerate advertisements. If you don't want to see ads and want additional features, there's no way around a monthly or annual subscription.

This freemium approach allows Duolingo to attract as many users as possible and, with the help of this large pool of users, to continuously develop its app thanks to A/B testing. Of course, having many users is also a good marketing tool when many of them talk to friends and acquaintances about their experiences with Duolingo.

The frequency of interactions with the platform increases when a monthly active user becomes a daily active user and then a subscriber who pulls out their credit card. Let's take a closer look at the path from user to subscriber.

Monthly users as marketing ambassadors and data pool

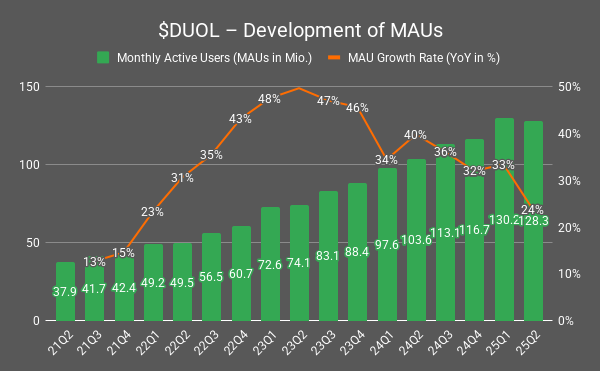

Since Q2 2021, the number of monthly active users (MAUs) has increased from 37.9 million to 128.3 million (Q2 2025).

This represents an impressive growth of 239% in total, or 35% per year. This trend in MAU growth is driven by a clear marketing message and a growing range of free learning content. Thanks to these high and growing user numbers, Duolingo can continuously collect more relevant data and thus improve its app.

From Q1-2025 to Q2-2025, the number of MAUs actually fell slightly from 130.2 million to 128.3 million. This was due to a very successful marketing campaign in Q1-2025, which brought many new users to Duolingo, but more on that later. Nevertheless, growth from Q4 2024 to Q2 2025 continues to show a positive trend.

Daily active users form strong habits

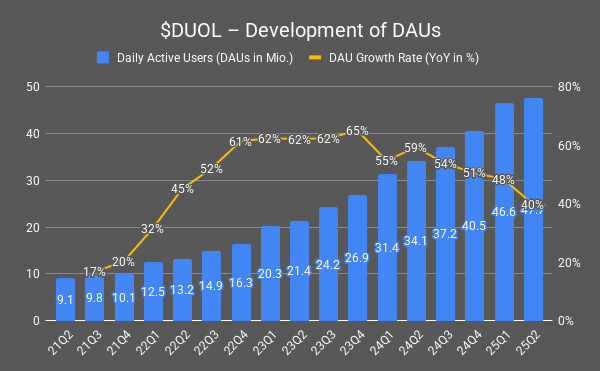

Even more important than MAUs are daily active users (DAUs), because they show how many users have made Duolingo a regular daily habit. And such daily habits are particularly valuable because habits tend to last a long time, and so does loyalty to Duolingo. Furthermore, daily learning also leads to better results for users, which underscores the added value of the app.

From Q2 2021 to Q2 2025, Duolingo increased its DAUs from 9.1 million to 47.7 million, which represents a total increase of 424% or 52% growth per year. That is truly outstanding growth.

Another positive aspect is that DAUs are growing in all regions, even in markets where Duolingo is already used by a large proportion of the population:

“One thing that is really interesting to say is that the growth rate per region is not really correlated with how mature each region is. So, for example, probably, our most mature region is Latin America, but it's also growing very fast.

That's actually growing at like 80% year over year. So, what that tells us is that we really are far from saturating any of our markets. We're growing pretty fast in all of our markets” – Luis von Ahn, co-founder and CEO of Duolingo, Q4 2024 earnings call

The company therefore still has a lot of growth potential ahead of it in terms of users.

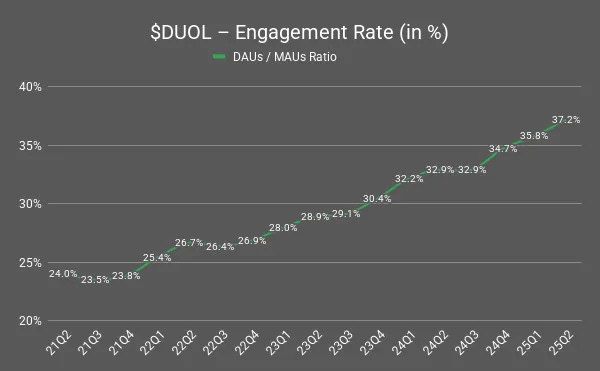

Continuous app optimization drives up engagement rates

Duolingo is thus able to increase DAUs even faster than MAUs. This is also evident in the engagement rate, i.e., the ratio of DAUs to MAUs, which climbed from 24% to over 37% (Q2 2021 to Q2 2025). More and more monthly active users are becoming daily users.

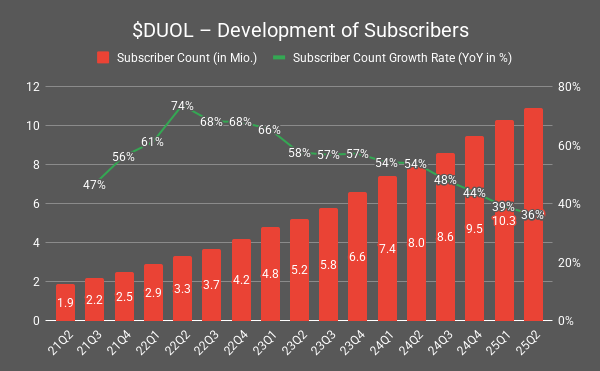

Subscriber count rises thanks to more functions and features

However, the core element is clearly the number of subscribers: since Q2 2021, the number of paying subscribers has increased from 1.9 million to 10.9 million (Q2 2025). This corresponds to strong growth of 474% in total and annual growth rates of 55%.

The main driver behind this was the increasing value of subscription membership thanks to more functions and premium features such as the AI tutor Lily, who gives you feedback on your answers or practices dialogues with you in role-playing games.

Since the introduction of video calls with Lily, which is essentially a GenAI-powered conversation feature, user interaction with the Duolingo Max subscription has increased significantly. The AI tutor Lily is deliberately sarcastic and cheeky because Duolingo uses this approach to make learning more exciting and entertaining. This humor is part of the brand and ensures that users come back regularly and enjoy learning.

In focus: High-priced “Max” subscription with AI tutor Lily

Duolingo wants to increase the number of subscribers, especially Max subscriptions. To this end, Duolingo CEO Luis von Ahn has provided some interesting insights into their strategy:

“The types of tests that we run are things like,

When do we advertise Max?

Who do we advertise it to?

Do we advertise to subscribers?

How often do we advertise it to subscribers?

What do we say when we advertise to them?

And we have found some vectors that really allow us to experiment a lot.

So, for example, one of the main ways we're getting people to subscribe to Max is with an ad for Video Call. We show kind of what it looks like to do Video Call, and that is very effective at getting people to subscribe.” – Luis von Ahn, co-founder and CEO of Duolingo, in the Q4 2024 earnings call

Growth potential through tapping into advanced learners

Duolingo also mentions that they have primarily focused on beginners when it comes to language learning and are now turning their attention to advanced learners.

In addition to word-of-mouth marketing, they are deliberately relying more on influencers to talk about the new courses for advanced learners. Users who want to learn English are particularly important here, as they account for around 80% of spending in the language learning market.

However, clearly less than 50% of Duolingo's revenue comes from English learners, which suggests further growth opportunities in this area.

“English learners are a pretty major opportunity for us. The reason for that is because if you look at the broader language learning market outside of Duolingo, the majority of the spend, about 80% of it is from people who are learning English.

But if you look at Duolingo, the amount of revenue that we make from people who are learning English is significantly less than 50%, so there's a major opportunity there. And the reason that we are underrepresented within the English learners is because we haven't historically had intermediate or advanced content in English.

We started working on that a few years ago. And by now, all of that content is there, so we're very happy with the content.” – Luis von Ahn, Q3-2024 Earnings Call

Interim conclusion on subscriber growth

Duolingo is gradually converting free users into paying subscribers.

The company is constantly improving in this area thanks to app optimization based on user data and more features in the app.

In particular, the AI tutor Lily helps subscribers practice their conversations anytime, anywhere. This is driving the adoption rate of the high-priced Max subscription.

II. Higher revenue per subscriber

Before we take a closer look at revenue per subscriber, I would like to briefly explain how important subscription revenue is for the company as a whole.

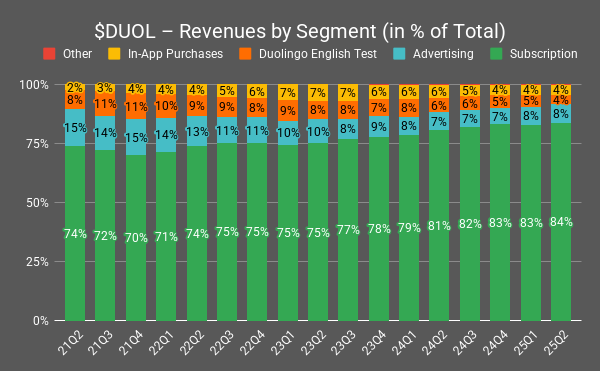

Specifically, Duolingo has five segments that contribute to the company's revenue. Here is a look at the breakdown of revenue in Q2 2025:

💳 Subscription: This is by far the largest segment, accounting for 84% of total revenue. What's more, the importance of this segment has actually increased: in Q2 2021, it accounted for 74% of revenue. Revenue here comes from the Duolingo Plus, Super, and Max subscription models. Users pay monthly or annually for benefits such as ad-free learning, offline mode, additional progress features, and (exclusive to Duolingo Max) the AI tutor Lily.

📺 Advertising: Around 8% of revenue is generated by advertising that non-paying users see in the free version of the app. Here, Duolingo uses a classic app monetization model via advertising networks such as Meta and Alphabet.

📝 Duolingo English Test (DET): This segment contributes about 4% to revenue. The English test costs around $59 per exam and is now accepted by over 5,000 universities worldwide. It is also gaining importance in areas such as immigration and the job market.

💰 In-App Purchases (IAP): Another 4% of revenue comes from the sale of virtual goods in the app, including gems, “streak freezes,” extra lives, and costumes for the mascot Duo (the green owl). Although this source of revenue is smaller, it provides a nice extra income.

🌮 Other: Accounting for less than 1% of revenue, this segment plays a negligible role. It includes smaller experiments such as the “Duo's Taquería” restaurant in Pittsburgh and merchandising activities.

In short, subscription membership revenues are the key factor in Duolingo's economic success, accounting for 84% of its total revenue. The rest is more of a nice-to-have.

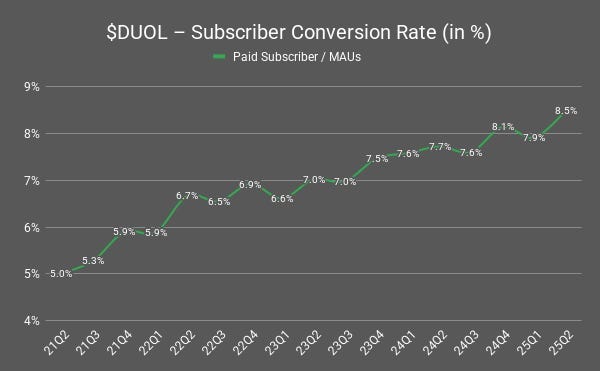

In my opinion, the subscription segment will account for an increasing share of Duolingo's total revenue in the future because the proportion of paying subscribers among MAUs is steadily increasing: specifically, the subscriber conversion rate rose from 5.0% (Q2 2021) to 8.5% (Q2 2025).

Of 20 MAUs in mid-2021, only 1 had a subscription, and the trend is that soon one in ten MAUs will be a paying subscriber. This is an extremely good figure, as most consumer apps, such as gaming and productivity apps, have very low subscription rates, often below 2% of all users.

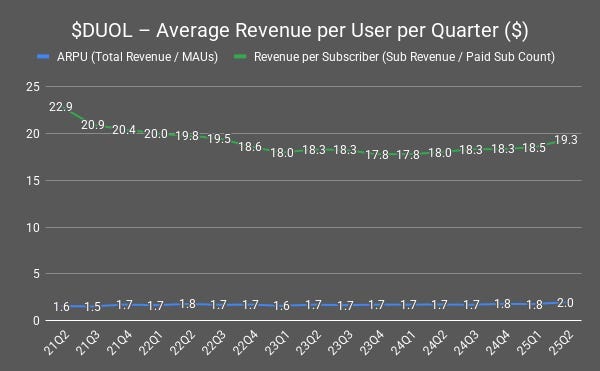

It is interesting to note in this context that the average revenue per subscriber per quarter at Duolingo ranges from $17.8 to $22.9 (Q2-2021 to Q2-2025). Revenue per subscriber fell gradually from $22.9 (Q2 2021) to $17.8 in Q4 2023, before rising again to $19.3.

In my view, there are several reasons for these fluctuations in revenue per subscriber:

The proportion of annual subscriptions is steadily increasing: The price of a monthly subscription to Duolingo is higher than the annual subscription (as is the case with many subscription models). Because the proportion of annual subscriptions is increasing compared to monthly subscribers, the average revenue per user is decreasing. This may appear to be a weakness in the short term, but I believe it is the right decision in the long term because annual subscribers stay longer than monthly subscribers. This means that more revenue per subscriber is generated over several years.

Global expansion puts pressure on revenue per subscription: In 2020, the price of a Duolingo subscription was the same worldwide, regardless of whether you lived in the US or India. Over time, Duolingo has adjusted this regionally to reflect people's purchasing power. This increases the number of subscriptions, even if the revenue per subscription decreases. Nevertheless, total revenue is increasing.

New Year's discounts reduce revenue per subscription: Duolingo often experiments with different pricing models (e.g., annual discounts, New Year's special offers). These reduce revenue per subscriber in the short term, but keep them loyal for longer, which increases revenue per subscriber over their “lifetime” (known as lifetime value or LTV).

Introduction of new pricing plans, most notably Duolingo Max: The more expensive Max subscription was launched in 2023 and has been growing steadily ever since. Adoption does not happen overnight, but builds slowly. According to Duolingo CEO Luis von Ahn, Max subscriptions accounted for 5% of all subscriptions a few quarters ago, then rose to 7% in Q1-2025 and now reached 8% in Q2-2025. The driver behind this is continuous product optimization. This trend also explains the gradual increase in revenue per subscription since the end of 2024, because Max now contributes more revenue per subscriber than “Super,” the company's other subscription model.

By combining growth in subscriber numbers and revenue per subscriber, Duolingo has been able to significantly increase its total revenue: since going public in 2021, revenue has climbed from $251 million to $748 million in 2024, which equates to a threefold increase in just three years.

Duolingo expects revenue of $1.157 billion for 2025 and states in its 2024 annual report that consumer spending on language learning is expected to grow to $123 billion by 2027. This means that Duolingo has a market share of less than 1% and therefore has a lot of growth potential ahead of it.

Interim conclusion on revenue per subscriber

In my view, revenue per subscriber will continue to rise in the long term because the added value of the subscription will increase and, in line with this, subscribers' willingness to pay for this added value.

In the short term, however, I assume that revenue per subscriber will not show too much momentum yet, because Duolingo prioritizes certain groups of users and subscribers (e.g., by region, willingness to pay, etc.).

The relevant goal is to maximize revenue per subscriber in the long term, not just in one or two quarters. Duolingo has already done this very successfully, for example, with annual subscription models.

III. Improvement in cost structure

Basically, subscription models (such as Duolingo's) are attractive to investors because they enable predictable revenues and are often highly profitable.

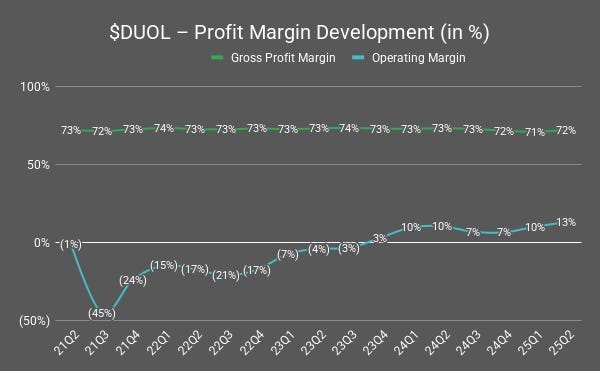

This is clearly evident in Duolingo's profit margins:

The gross margin is extremely stable and high. Each additional download of the app incurs virtually only hosting costs and app store fees for Duolingo. For Max subscriptions with AI tutor Lily, there are additional API costs for GPT queries, which are steadily decreasing, however. The Duolingo Max subscription therefore generates more gross profit per subscriber, but a lower gross margin than Super subscribers due to the higher costs of these AI queries. All other costs (such as marketing, administration, or research) are covered by operating expenses (OPEX). As a result, the gross margin has remained consistently high at 71% to 74% since Q2 2021, with only minimal fluctuations.

The operating profit margin (EBIT margin) is calculated by subtracting operating expenses (OPEX) from the gross margin. And here you can see a huge improvement: this margin was still negative at 45% in Q3 2021. It was not until Q4 2023 that Duolingo became operationally profitable with a 3% margin. Now the EBIT margin stands at a solid 13% (Q2 2025).

Why did Duolingo take so long to become profitable?

Quite simply, Duolingo first had to invest heavily in technology and content in order to be able to support and operate a platform of this size. For years, the company deliberately avoided aggressive monetization in order to attract and retain users.

Today, it is clear that this patience was the right approach, because the broad user base is the foundation for sustainable profitability.

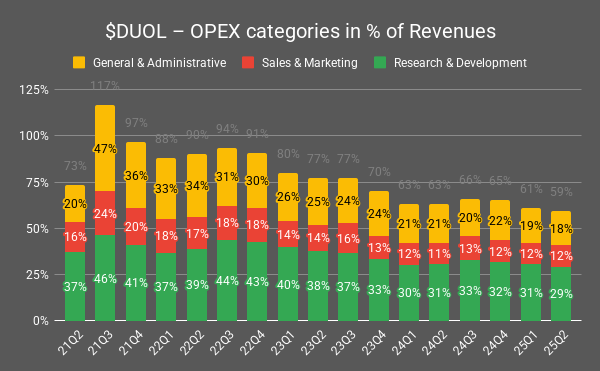

Let's take a closer look at operating expenses (OPEX) to better understand their structure and development. Duolingo divides its OPEX into three categories:

🟩 Research & Development (R&D) accounts for the lion's share of OPEX costs. This includes almost everything related to products, apps, and new subjects (math, chess, music, etc.), primarily personnel costs for software developers, product experts, and data scientists. From 2021 to 2025, the share was quite high: between 29% and 46% of revenue. In Q2 2025, it is 29%. This means that Duolingo continues to invest heavily in product development, but the share is declining as revenue increases.

🟥 Sales & Marketing (S&M) consists of performance campaigns, influencer partnerships, and experiments on TikTok. Historically, these costs have ranged from 11% to 20% of revenue. In Q2 2025, S&M was at 12%, which is toward the lower end. This shows that Duolingo is growing largely organically; in the US, for example, Duolingo does not use paid marketing. Instead, viral campaigns on social media and word-of-mouth advertising lead to high and cost-effective brand awareness.

🟨 General & Administrative (G&A) primarily includes costs for personnel in the areas of management, finance, and human resources. G&A used to be a pretty big cost item (even over 40% in 2021 because of the IPO and the costs that came with it). But now, it's way down as a percentage of revenue, and in Q2 2025, it'll only be 18% of revenue.

Duolingo's operational cost structure: From chaotic to efficient

Generative AI will help Duolingo further improve its cost structure in three ways:

General efficiency within the company: all Duolingo employees use AI tools in their daily work to be more productive. This should lead to a long-term reduction in total operating expenses (OPEX) in relation to revenue.

New features: The example of video calls with AI tutor Lily shows how AI is enabling the next step toward personalizing learning content. Such features increase engagement and subscription retention, which should have a positive effect on the number of subscribers.

Generation of learning content: 100% of the content on Duolingo is now created using AI. In fact, the pace is increasing massively as a result: whereas Duolingo previously needed 12 years to manually create 100 courses, today they only need 1 year for 48 new courses. Thanks to AI, Duolingo is now 5 times faster than before. This works particularly well because Duolingo can already build on a huge pool of manually created content. As a result, content production is becoming faster and cheaper. This should lead to a decline in R&D costs in relation to revenue.

I see content creation as a particularly important issue here: the associated costs fall under the R&D category. Precisely because this category is heavily dependent on personnel costs, I believe that Duolingo can produce more content faster per employee thanks to AI.

As a result, I expect R&D costs to gradually decline in relation to revenue. This is especially true because, thanks to AI, Duolingo will be able to generate 10 times more content in 2024 than it did in 2022:

“We're definitely investing in AI to automate things inside the company. What that does is that actually decreases costs. That's good.

And it also allows us to go way faster, particularly in content creation. So, the amount of content we're able to generate compared to two years ago is way more. I mean, it's like 10x or more than that. So, that's one thing.” – Luis von Ahn, Q4-2024 Earnings Call

However, in order to implement these and other significant improvements, Duolingo must first invest more money. After all, nothing comes from nothing. It is important to understand that many of these costs are upfront costs: the costs are quite high at the beginning to set everything up, but will decrease after 2025 once everything is in place.

“So, the way to think about it is there's going to be kind of an upfront cost for AI, which will happen probably throughout this whole year, but it's because we're in a unique opportunity, a unique time in history where we really want to develop the best possible AI features over time.” – Luis von Ahn, Q4-2024 Earnings Call

Interim conclusion on improving the cost structure:

The OPEX ratio has fallen from over 100% of revenue (2021) to just 59% in Q2 2025.

This is a sign of classic operating leverage: cost blocks (developer teams, marketing, and administration) do not grow at the same rate as revenue, but are primarily fixed costs. This positive trend should continue in the long term, although I expect a short-term counter-movement in 2025 due to higher investments in AI.

With a growing user base and higher subscription revenues, Duolingo will automatically become more profitable as costs rise at a slower rate.

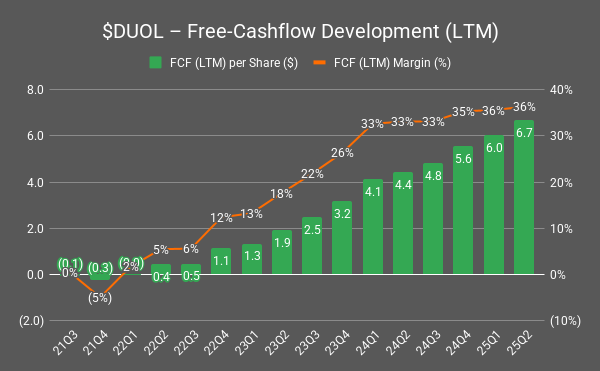

IV. Increase in free cash flow per share

For me, one of the most important key figures is free cash flow (FCF) per share. FCF indicates how much money a company actually has in its account at the end of the day after deducting investments. And looking at it at the share level helps to understand how much cash a company actually generates for you and me as shareholders.

By way of comparison, net earnings per share (EPS) is ultimately primarily an accounting figure. Net earnings include many effects that do not involve any cash flow.

A simple example: A company buys an office building for $10 million and depreciates it over 40 years. As a result, $250,000 in depreciation appears in the income statement each year ($10 million / 40 years). But in reality, not a single cent leaves the company during these years because the cash outflow only occurred at the time of purchase, which is only recorded in the cash flow statement (and not in the income statement).

Such effects show why the reported profit does not necessarily say anything about the actual cash flow and must be viewed in the context of other key figures and the life cycle of the company.

This is precisely where free cash flow comes in: it filters out purely accounting items and shows how much money actually remains in the coffers at the end of the day. In other words, what really benefits us shareholders.

I like to look at FCF per share over the last 12 months (LTM) because this reduces the impact of outliers and special effects in individual quarters and makes the trend smoother and more meaningful.

At Duolingo, FCF per share (LTM) has risen from -$0.1 in Q3 2021 to +$6.7 (Q2 2025). FCF has been positive since Q2 2022 and is now in the green. Year-on-year alone, FCF has skyrocketed by over 52%.

According to this, Duolingo is currently valued at around 45 times its FCF for the last 12 months. At first glance, this seems high, but we will come back to this later in the valuation analysis.

Since mid-2021, the share of free cash flow in revenue (FCF margin) has increased from around 0% to an impressive 36%. This is a very encouraging development.

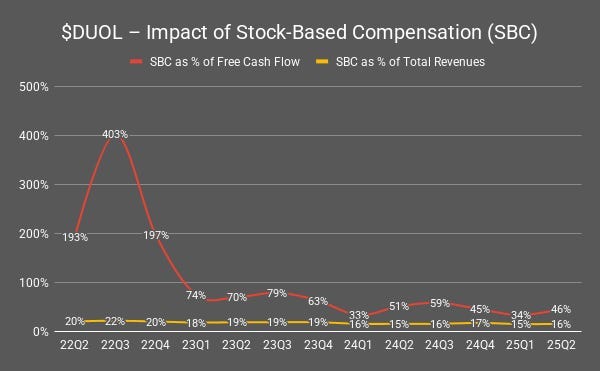

However, it is also important to note that Duolingo relies heavily on stock-based compensation (SBC) for its employees in order to motivate them in the long term. This SBC leads to the issuance of new shares to reward employees for their performance and retain them with the company. As a result, from a shareholder's perspective, SBC dilutes our share of the company's free cash flow pie.

This is particularly critical when the SBC is disproportionately high. At Duolingo, the SBC has been very high in relation to free cash flow in the past. I have deliberately excluded the 2021 period here because there were some special effects due to the IPO that distort the overall picture.

Since Q2 2022, SBC as a percentage of FCF has fallen from 193% to 46%. So it is still high, but clearly on a downward trend. In relation to revenue, SBC also fell from around 20% (Q2 2022) to 16% (Q2 2025), which is a positive development.

Interim conclusion on free cash flow per share:

Duolingo has only achieved positive free cash flow (FCF) on a 12-month basis since Q2 2022. This is because the company is still in the early stages of monetizing its platform.

The drivers for FCF are (1) growing subscriber numbers combined with (2) rising revenue per subscriber plus (3) optimization of the cost structure, in particular operating expenses (OPEX), which are falling as a percentage of revenue.

The relatively high share-based compensation (SBC) is critical and should be deducted from FCF in a conservative assessment.

Although SBC creates the right incentives to motivate and retain top talent at Duolingo, it also dilutes our share in the company as shareholders. However, SBC is declining in relation to revenue and FCF, which is welcome news.

I expect these favorable developments to continue as Duolingo grows as a company. This is because a large part of Duolingo's cost structure consists of personnel costs and the associated SBC. With or without SBC, Duolingo will be able to significantly increase its free cash flow per share in the coming years.

In addition to the financial improvements, which can be easily measured quantitatively as output, there are also qualitative reasons and hidden input factors that are leading to this turning point in the company's history.

3) Turning point thanks to new areas accelerated by AI

I believe that the turning point for Duolingo will come when one of the new subjects or areas (mathematics, music, and chess) contributes more than 10% to total revenue and reaches profitability thanks to optimized monetization. This is because the fundamental improvement will then also be visible in the financial figures, and the stock market will reward this with rising prices.

Duolingo can only implement these improvements because the company has exceptional organizational characteristics. To better understand the development of these characteristics, let's first take a look at the company's history:

Duolingo was founded in 2011 by Luis von Ahn and Severin Hacker. Both had earned their PhDs in computer science at Carnegie Mellon University in Pittsburgh.

The key figure here is clearly Luis von Ahn, who was already well known at the time: in 2009, he sold his startup reCAPTCHA to Google. The amount was never officially confirmed, but is estimated to be between $25 and $30 million.

You're probably familiar with reCAPTCHA: those little images on the internet where you have to click on traffic lights, crosswalks, or fire hydrants to prove you're not a bot.

After selling reCAPTCHA, Luis could have comfortably retired or become a professor. But he wanted more. The topic of education was extremely close to his heart.

Growing up in Guatemala, Luis experienced firsthand how access to a good education determines opportunities in life. His single mother invested everything in his schooling, which enabled him to study in the US. Language was the key that shaped his future.

It was precisely this motivation that gave rise to the idea for Duolingo: making education accessible to everyone, free of charge.

Together with co-founder Severin, he built an app that would give everyone around the world the opportunity to learn languages and thus gain access to better prospects. The business model behind it was clever from the start: the basic version is still free today, and as already mentioned, the company finances itself through advertising and, above all, subscriptions.

Especially the company's mission is a key piece of the puzzle for success: making education accessible to everyone. Co-founder and CEO Luis von Ahn is clearly committed to this mission, as he clearly stated in the S1 filing for the IPO in 2021.

It is precisely these kinds of missions that attract and retain top talent. Money is not the only motivator, especially for top talent, who regularly receive many great job offers with generous compensation packages.

This mission is the foundation that has created the company's unique corporate culture. And it is precisely this culture that has helped the company achieve its strong market position and clear competitive advantages, which are misunderstood by the stock market. I will therefore explain this in more detail in the next section.

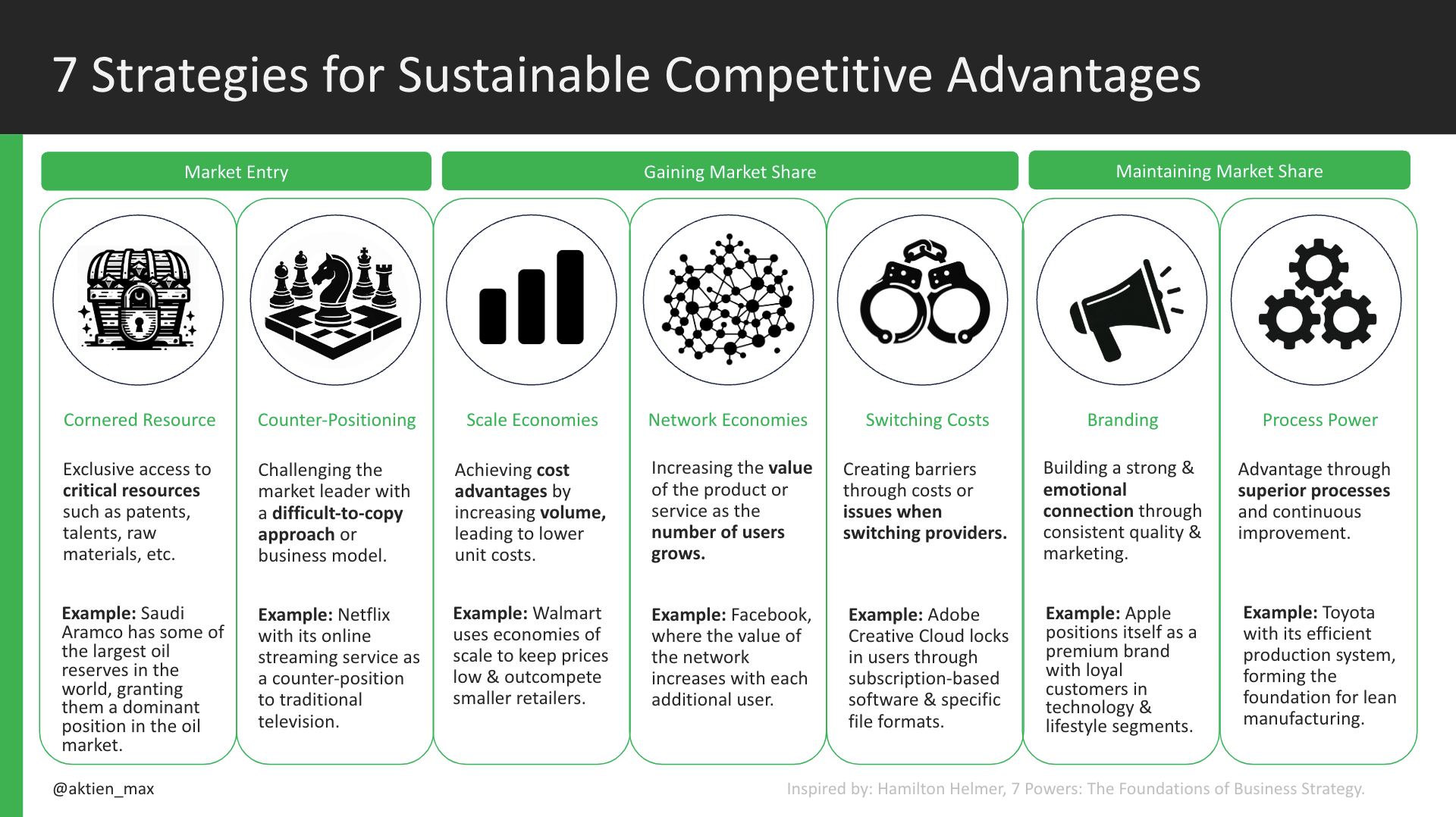

4) Competitive advantages in detail (7 Powers)

Duolingo is particularly notable for its experimental corporate culture, which leads to constant product improvements at record speed. Over time, this has resulted in seven competitive advantages that few competitors can replicate:

Cornered Resource 💎

Counter-Positioning ⚔️

Scale Economies 📈

Network Effects 🔄

Switching Costs 🔗

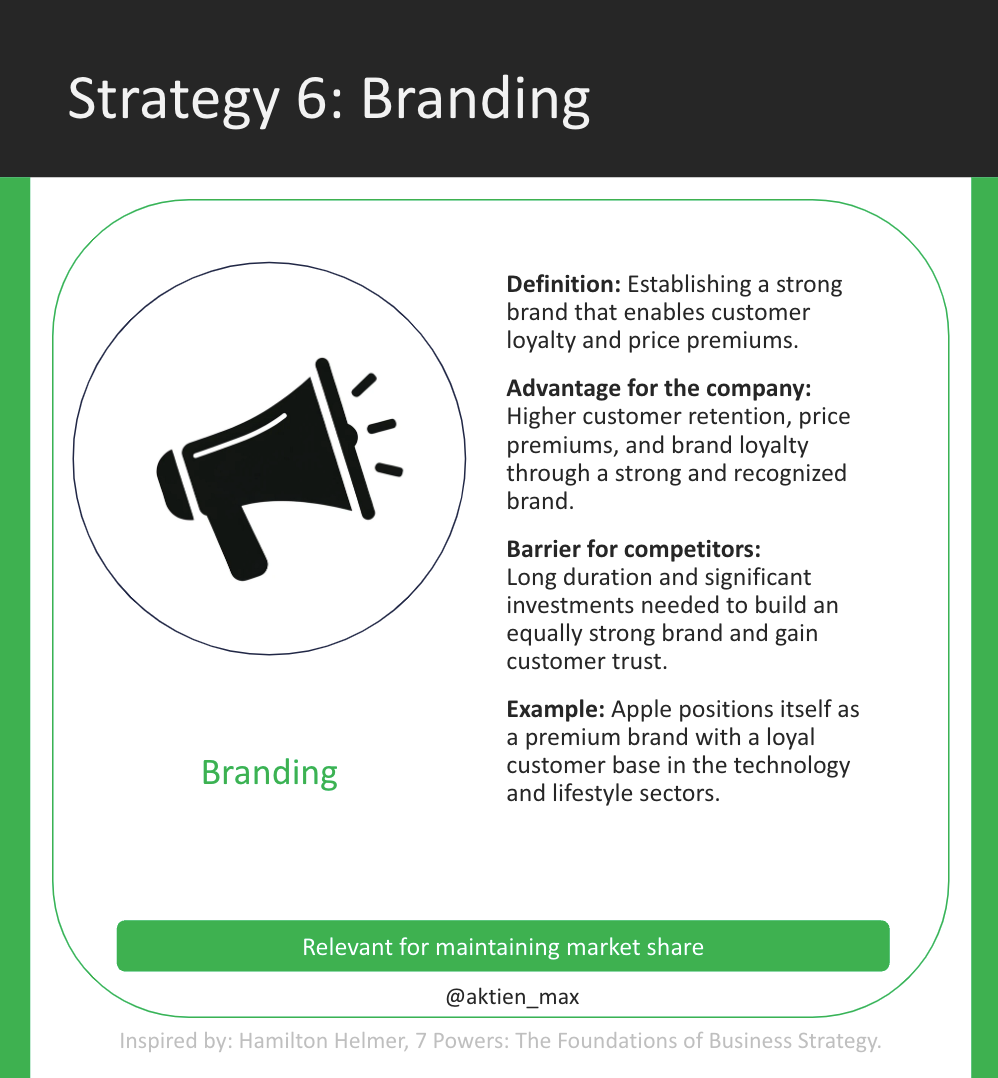

Branding 📣

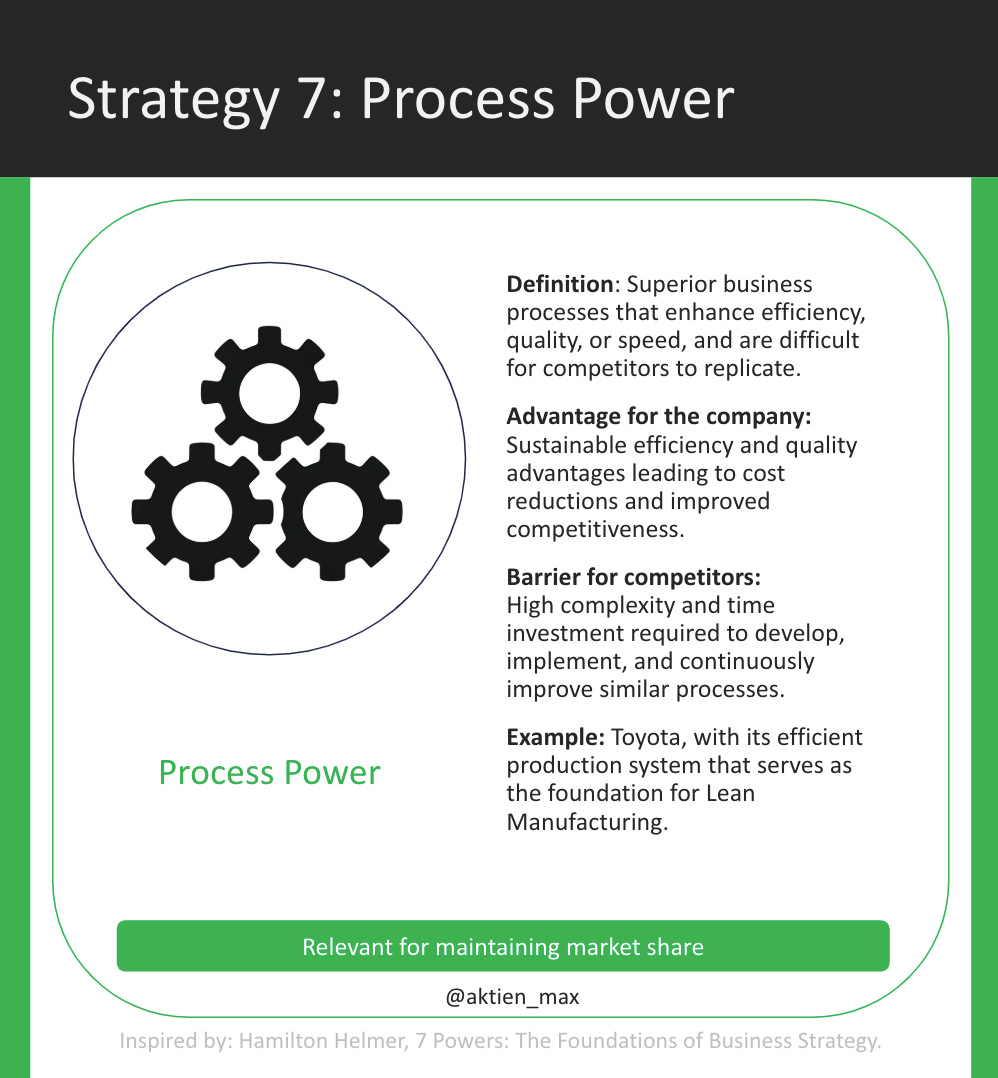

Process Power ⚙️

As a concept for assessing competitive advantages, I use the “7 Powers” from Hamilton Helmer's book of the same name, which is well worth reading.

A power offers a company an economic competitive advantage (e.g. a larger market share or higher profit margins than the competition) and at the same time represents a hurdle for competitors to also achieve this economic advantage.

Let's look at these 7 moats in detail:

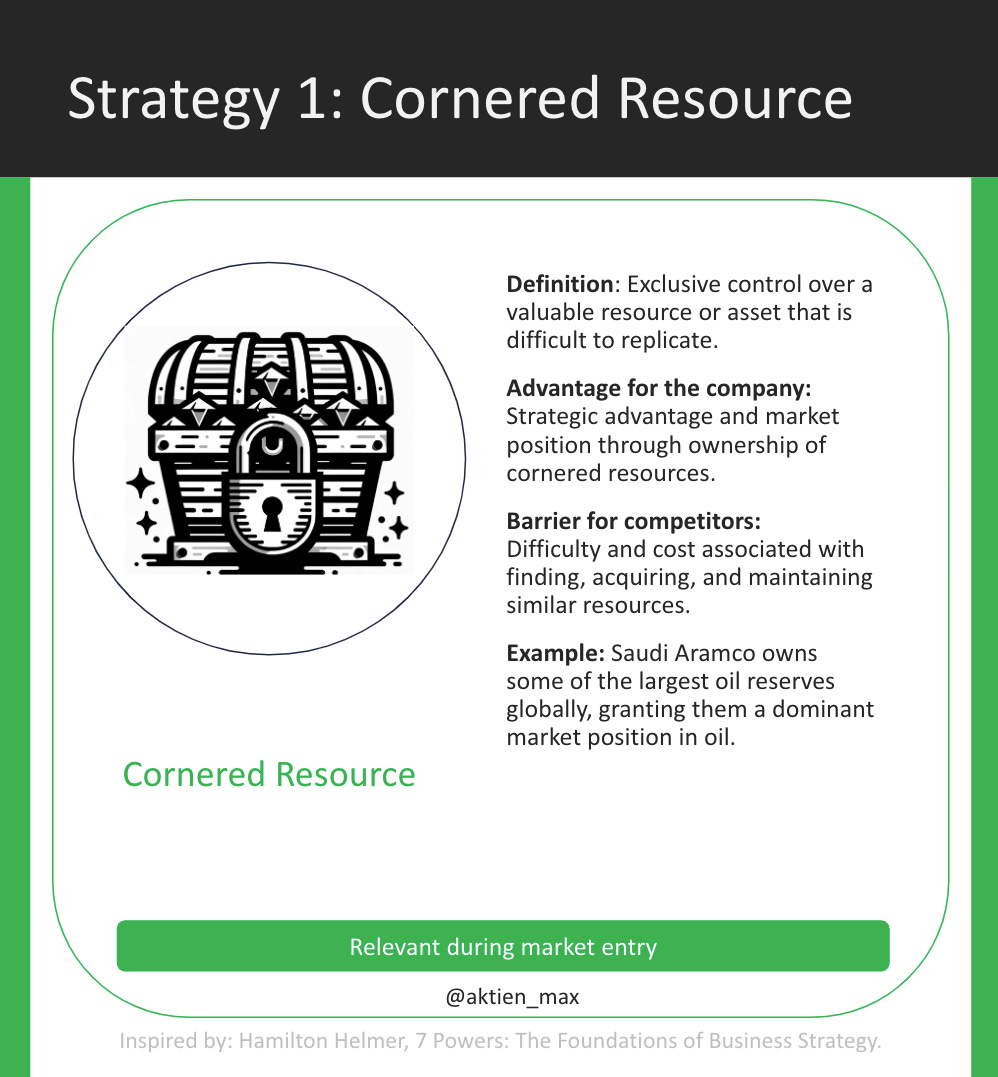

I. Cornered Resource thanks to unique data treasure trove 💎

One key advantage of Duolingo is the huge treasure trove of data that the platform generates every day. With over 128.3 million monthly active users and 47.7 million daily users (Q2 2025), it has created a database that is unique in the education sector.

This gives Duolingo billions of dollars worth of proprietary language learning data that no generic AI model such as ChatGPT, Gemini, or Perplexity can replicate. While generative AI is based on general internet data, Duolingo's database is tailored precisely to the use case of language learning.

The company's in-house AI model, Birdbrain, works in tandem with generative AI (such as ChatGPT):

BirdBrain ensures that every user gets exactly the right exercise at the right time. The database for this consists of billions of daily interactions, mistakes, and successes. Over 1 billion exercises are completed every day. Each of these exercises provides valuable data points for BirdBrain, Duolingo's in-house machine learning model. BirdBrain continuously calculates which tasks are at the right level of difficulty for each individual user. This daily fine-tuning ensures a learning experience that continuously improves.

Generative AI (e.g., ChatGPT in Duolingo Max) comes into play whenever open conversations are involved—such as in role-playing games or video calls with AI tutor Lily. This requires models that can conduct realistic dialogues. Generative AI now also helps with the creation of new exercises for classic course content, but not in an uncontrolled manner: everything runs through Duolingo's own framework and is reviewed by language experts.

In combination, this means that BirdBrain determines the what (which exercise, when), while ChatGPT & Co. deliver the how (linguistic content, realistic dialogues, AI-supported conversations). The result is a system based on unique data that integrates generative AI into learning processes in a targeted manner.

For example, generative AI can now generate better learning content for math, which, in combination with Duolingo's proprietary learning data, makes a big difference:

“(…) for generating content for math, the improvements in the models actually help because if you remember kind of a year ago, the models simply couldn't do math. Today, the models can do math, so we're able to generate more math content.” – Luis von Ahn, Q2-2025 Earnings Call

The progress of AI is particularly evident in Lily, which is available exclusively with a Max subscription. In the Q1 2025 call, Luis von Ahn describes how Duolingo benefits from the rapid advancement of large language models. Not only in terms of quality, but also in terms of cost:

“Improvements in latencies certainly help. But also improvements in the model. One of the things that really helps us is whenever a new model comes out, what happens is that the previous one, they just lower the price. So that helps us a lot. Maybe we don't use the latest one, but we are using the still the same one, but the price just came down. (…)

Now in terms of video call, we're doing a number of things to make it more engaging. For example, we are training our own, fine-tuning our own models to make it more engaging. (…)

It's just the conversations are going to flow a lot better, and they're going to adapt to your level a lot better. We're seeing basically changes on a weekly basis on that.”

Interim conclusion on cornered resources 💎

Thanks to its enormous user data, Duolingo has an unparalleled treasure trove of data that enables personalized learning every day via BirdBrain.

At the same time, the company uses external models such as ChatGPT, but integrates them with its own framework and proprietary data to build a clear competitive advantage.

This allows Duolingo to create not only better content but also realistic conversations with AI tutor Lily.

I therefore consider this competitive advantage to be very strong.

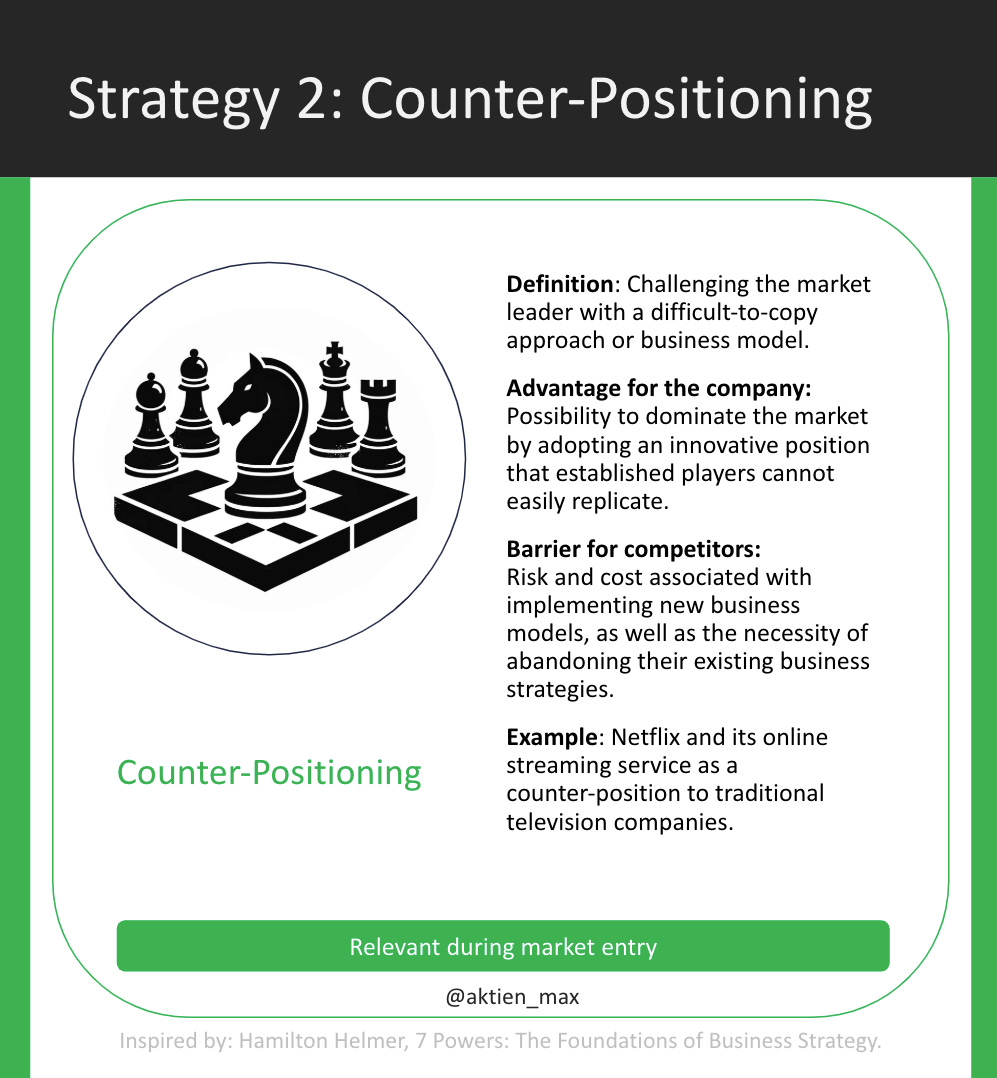

II. Counter-positioning through a pure app approach versus human language teachers ⚔️

Traditional language schools (Berlitz, Babbel Live, Preply, etc.) rely on costly teachers. Education is generally heavily dependent on human resources and therefore tends to be quite expensive in many countries. Duolingo, on the other hand, clearly positions itself as a free, mobile-first provider with gamification and AI.

An app that works better than a real teacher? Sounds unrealistic at first. However, studies show that Duolingo learners progress twice as fast in reading and listening comprehension as US students in traditional language courses:

“Our A/B testing has demonstrated that BirdBrain-powered experiences drive superior learner engagement and stronger learner outcomes. And research validates the efficacy of our product: Duolingo learners who complete five Units of Duolingo French and Spanish courses earn reading and listening proficiency scores comparable to those of US university students at the end of their fourth semester of language courses,

and in about half the time.” – Duolingo S1 filing for initial public offering

Even more exciting: Duolingo reaches target groups who have never learned a language before. According to management, this applies to around 80% of all users in the US:

“(…) for example, in the United States, about 80% of our users are people who were not in the market before. They weren't learning a language. So we just don't see that anything is -- there's nothing that we see that is pointing us to some like cap or anything like that.” – Luis von Ahn, Q3-2024 Earnings Call

With its focus on apps and untapped customer groups, Duolingo is even ranked number one among education apps worldwide and has been the highest-grossing app in this category since 2019.

Interim conclusion on counter-positioning ⚔️

Duolingo has successfully positioned itself as a free, mobile, and AI-powered alternative to traditional language schools, which often require expensive teachers.

Despite initial skepticism, studies show that Duolingo learners progress twice as fast in reading and listening comprehension as students in traditional US language courses.

In addition, Duolingo reaches many users who have not previously used language courses, thus significantly expanding the market.

With this innovative app approach, Duolingo has held the top position as the world's highest-grossing education app since 2019.

I consider this power to be distinctive, but it is not impossible to replicate. New competitors in particular are better able to replicate this advantage than established players in the market, who often still base their business model on traditional teachers.

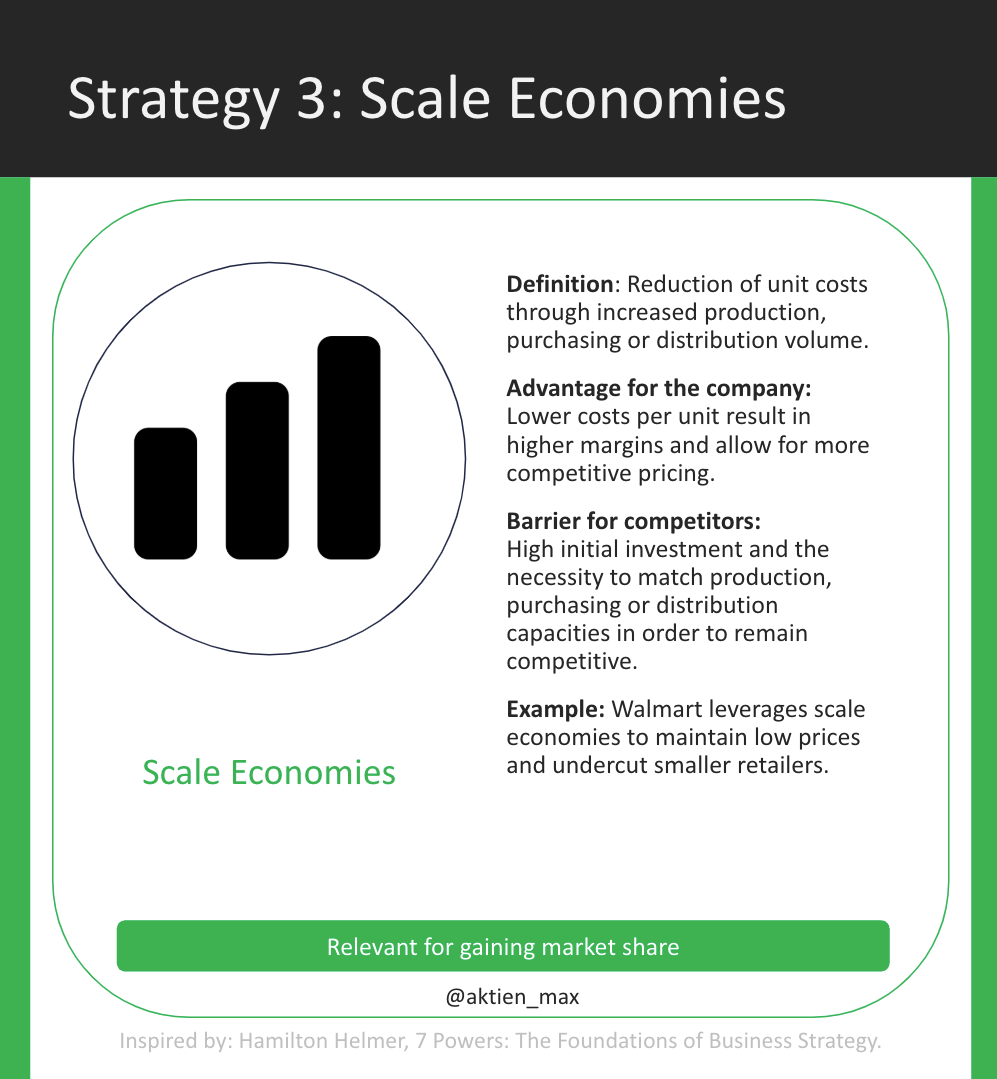

III. Economies of scale through growing size 📈

Software and platform models such as Duolingo benefit greatly from economies of scale as they grow in size:

This is precisely because Duolingo's cost structures have a clear fixed cost block for learning content and tech infrastructure.

The larger the app becomes, the lower the cost per app use.

After all, each additional user costs virtually nothing, so the potential for increasing profit margins is high.

Although Duolingo's gross margin is very high at 72% (Q2-2025), as already mentioned, the company is pursuing an approach that I have already explained in my Deep Dives on Hims & Hers and Tesla: Scale Economies Shared.

💡 Please note: With "Scale Economies Shared", a company benefits from falling unit costs due to higher unit volumes and passes on some or all of these savings to its customers in the form of lower end prices. This creates a positive feedback loop: More demand leads to even lower costs and further price advantages. As a rule, this increases customer loyalty and satisfaction.

A good example of this is that CEO Luis von Ahn does not want to keep the AI tutor Lily exclusively in the high-priced Max subscription model in the long term. As the inference costs per AI query decrease, he wants to make this feature available to larger customer groups. Some features may even be offered free of charge in order to attract even more users.

“Generally, we have these three tiers. We have the free tier. We have the Super, and we have the highest tier, Max.

At the moment, because of inference costs, particularly for Video Call, we have to have Video Call in the highest tier. That's not necessarily going to always be the case. It may be the case that, at some point, it gets cheap enough for us to put in a lower tier. We may even be able to give some of it for free.” – Luis Q4-2024, Earnings Call

Especially when the price of the Max subscription is falling thanks to declining inference costs per AI query, this would lead to a significantly higher adoption rate. This is particularly true in populous countries such as India, where incomes are also lower.

„But for example, in India, the price, I believe, is $70 a year, and that's too expensive for India. And we know that.“ – Luis Q4-2024, Earnings Call

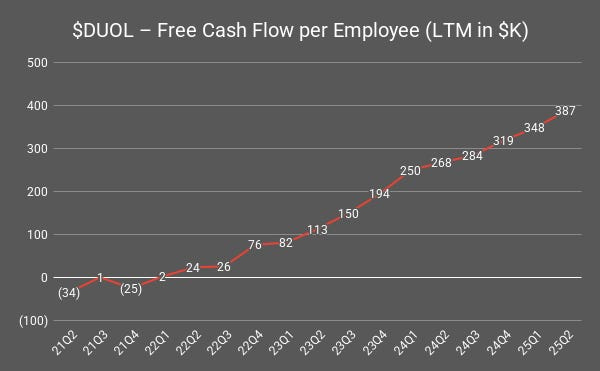

The growing economies of scale at Duolingo are reflected in the free cash flow per employee metric: this demonstrates the strength of Duolingo's business model, as it can generate steadily more cash per employee.

In Q2 2025, Duolingo generated $387,000 in free cash flow per employee, based on the last 12 months. Three years ago (Q2 2022), it was a meager $24,000, so the trend is clearly upward. This is very impressive for a company that employs just over 800 people.

Interim conclusion on economies of scale 📈

Duolingo effectively utilizes economies of scale, as fixed costs are distributed across more users, thereby reducing the cost per use.

The company passes on some of the cost savings to customers, for example through lower prices or free features, which promotes demand and customer loyalty. One example is the AI tutor Lily, which is to be made available to a wider range of users thanks to falling AI costs.

I also see this competitive advantage as very advanced here.

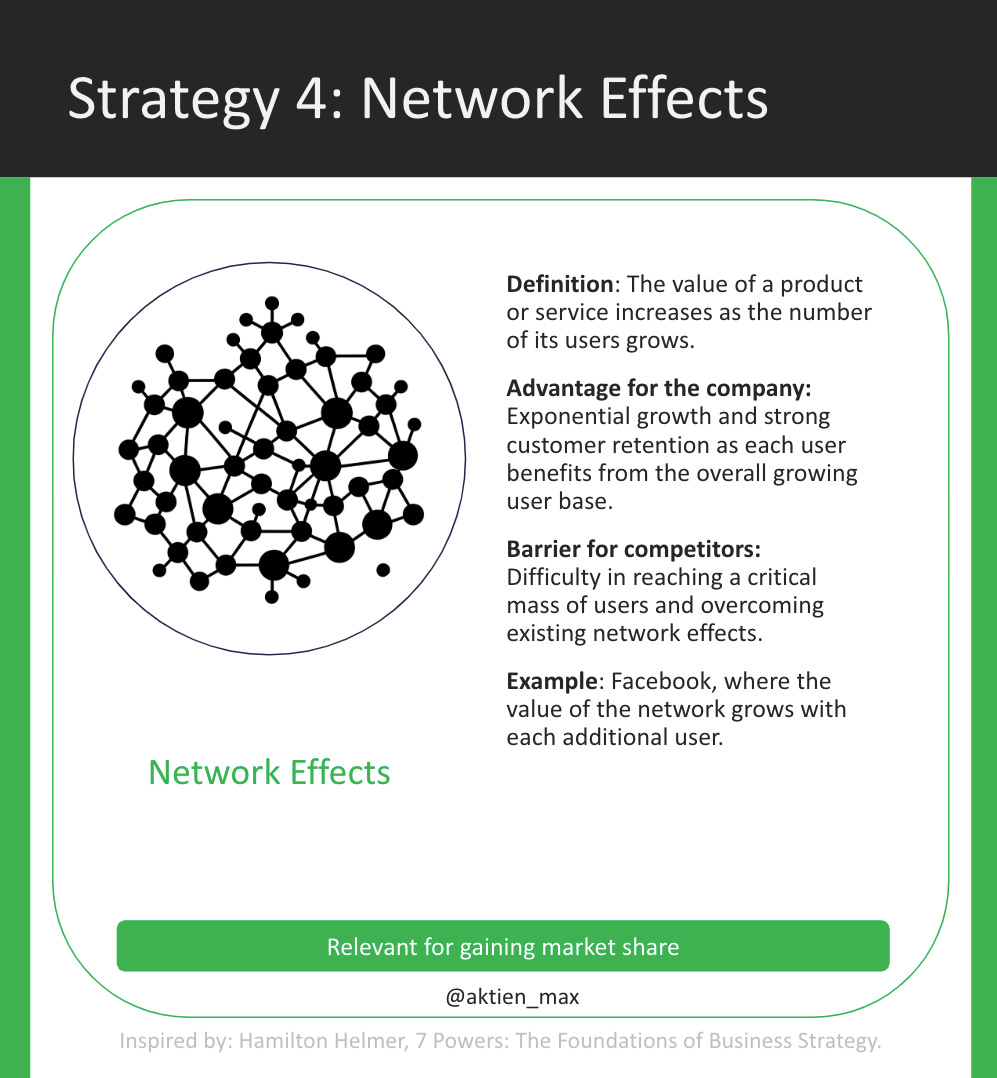

IV. Network effects through data-driven individualization 🔄

In my opinion, there are no classic network effects at Duolingo because learners do not benefit directly from each other.

However, there is an indirect network effect via the collected data, which improves and personalizes the AI, which in turn optimizes the app and attracts more users.

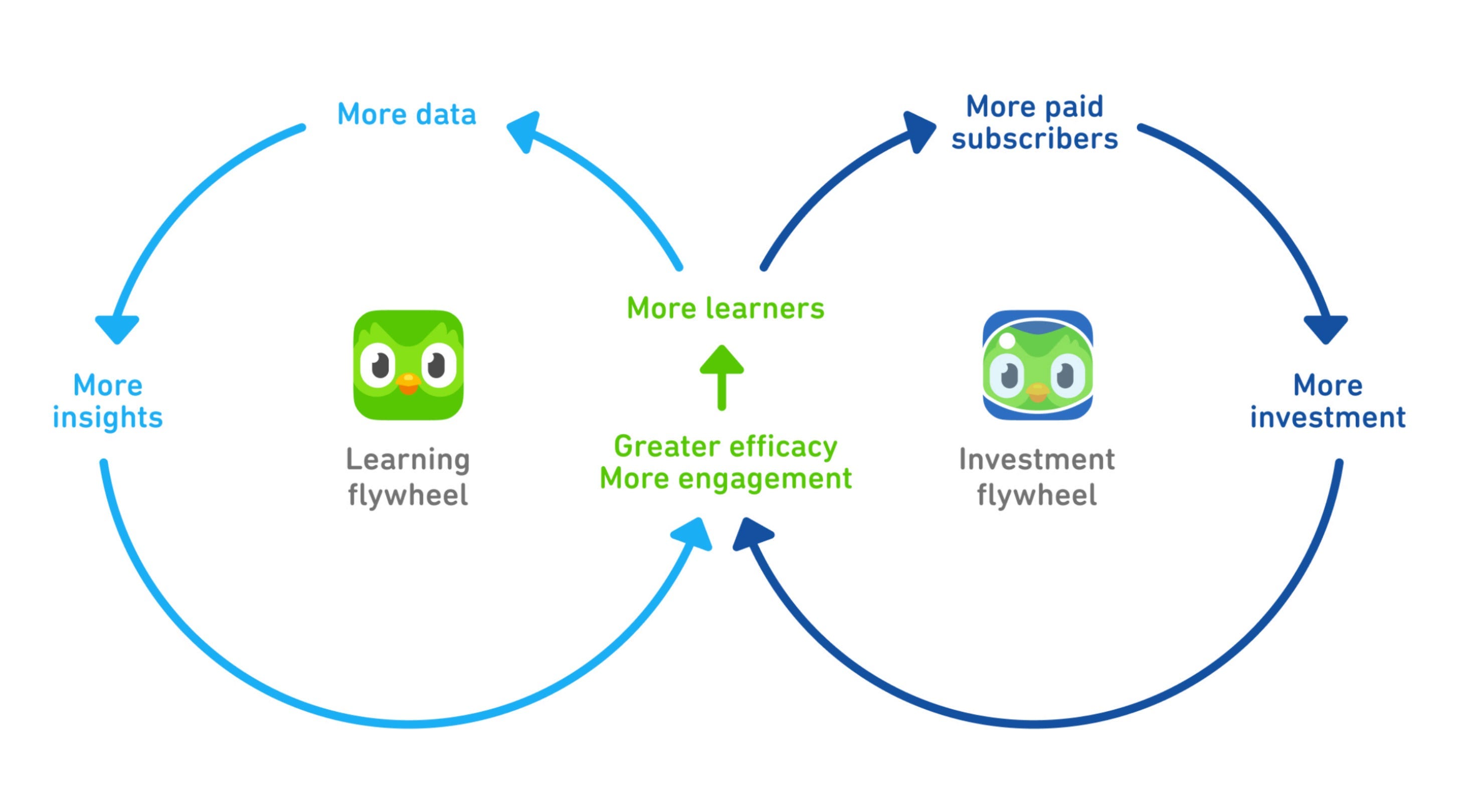

Duolingo itself refers to this as a “learning flywheel” and “investing flywheel.”

Duolingo's growth is based on these two flywheels, which drive each other:

Learning Flywheel: The more people use Duolingo, the more data the platform collects. This data flows directly into better courses, smarter AI (BirdBrain), and greater learning success. This is where network effects come into play: every additional user improves the experience for everyone else because the system can predict more accurately what works and what doesn't. This then results into more fun, more motivation, and thus more organic growth through word of mouth.

Investment Flywheel: Because Duolingo grows predominantly organically, they hardly have to invest money in expensive marketing. Instead, capital flows into the product, AI, and content. The more users upgrade to Premium, the larger the budget for innovation becomes, which further improves the learning experience. And the better the app gets, the more users join, which in turn reinforces the network effect via data and community.

In my opinion, it is the AI tutor Lily feature that will drive the 2 flywheels. The better and more human Lily becomes, the more the feature will be used and users will tell their family and friends about it, which will attract more users:

“Lily is not necessarily your best friend yet. (…) She'll remember what you told her last time. She'll ask you about your problems, etc. And we're working on that.” – Luis von Ahn, Q4 2024 Earnings Call

Interim conclusion on network effects 🔄

Duolingo does not have classic network effects like social media platforms, but it does have a powerful data-driven lever: every user improves the system for everyone else through their interactions.

The AI tutor Lily in particular could become a catalyst: the more human she appears, the more she drives both flywheels and thus the network effect.

The end result is a self-reinforcing cycle in which user growth, data, product quality, and monetization work together, and the moat widens from quarter to quarter.

Therefore, I consider the network effects at Duolingo to be pronounced, but not as strong as at Meta or LinkedIn, for example.

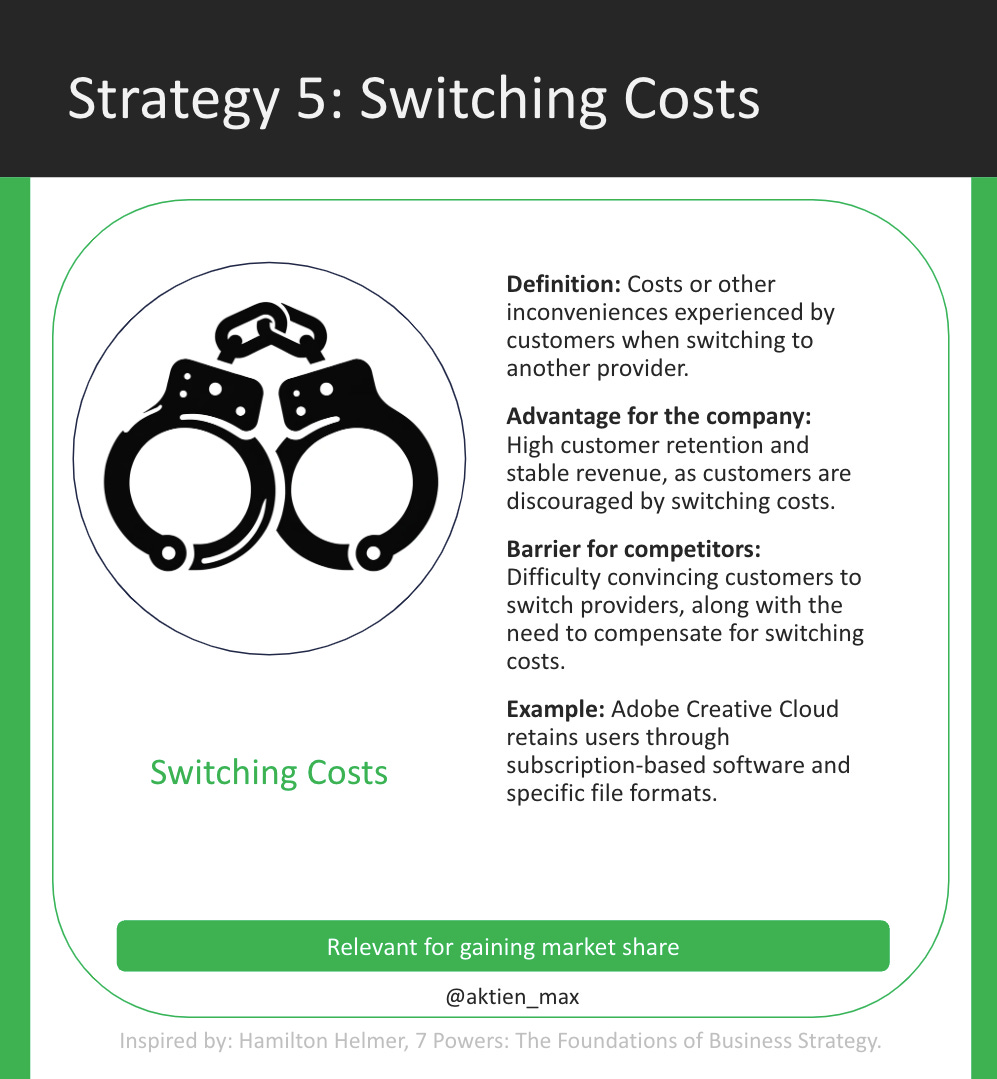

V. Switching costs thanks to personalization, social status, and subscription loyalty 🔗

The switching costs at Duolingo are not as high as they are for an ERP system from SAP, for example. Nevertheless, Duolingo deliberately creates barriers that make it difficult to leave.

On the one hand, the subscription model ensures loyalty. Annual subscriptions in particular, and family subscriptions even more so, bind several users at the same time. It is more difficult to cancel when the whole family is learning together.

Another factor is increasing personalization. Each user has their own learning model that knows exactly which tasks are suitable based on all their past mistakes and successes. This creates individual learning paths that users want to continue.

“We know every exercise you've done on Duolingo, whether you got it right or wrong. And if you got it wrong, we know the most likely piece of practice you need to learn from your mistake. And we use that data to make a model for each user. So when you start a lesson on Duolingo, we use artificial intelligence to pick exercises that are just right for you.” – Luis von Ahn, Q3-2021 Earnings Call

In addition, gamification features such as learning streaks, leaderboards, and virtual items increase the psychological and social switching costs. Anyone who has built up a streak of over 500 days or is high up in the global leaderboard will think twice about giving it up.

Interim conclusion on switching costs 🔗

Duolingo builds switching costs on several levels: annual and family subscriptions bind users financially, and personalization creates individual learning paths that you would lose if you switched.

Added to this are gamification features such as streaks and leaderboards, which create a kind of social and psychological incentive for long-term app use.

All in all, this creates a mix of financial, personal, and social barriers that keep users with Duolingo in the long term. However, in my opinion, the switching costs have only been moderate so far.

VI. Branding through community and word of mouth 📣

Duolingo has built one of the strongest brands in the educational technology (EdTech) sector. The green owl “Duo” has long been part of pop culture—countless memes, TikToks, and campaigns have made the brand famous worldwide.

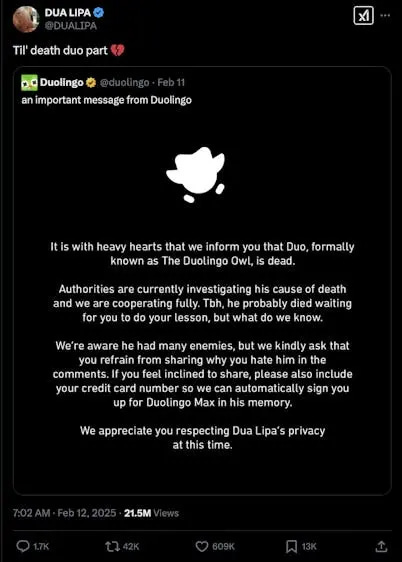

The “Dead Duo” campaign is the best example of this:

On February 11, 2025, Duo “died” in a viral marketing stunt. A revival challenge asked users to collect 50 billion XP to bring back the green owl.

The goal was not only achieved but exceeded: 50.9 billion XP – or around 5 billion lessons – were completed in just a few weeks.

The whole thing generated 1.7 billion impressions, with almost no advertising budget.

By comparison, the campaign even beat Doritos' expensive Super Bowl ad in terms of reach. Even mega-influencers like singer Dua Lipa (10+ million followers on X) promoted Duolingo for free, generating over 21 million impressions.

Other marketing experiments also strengthen the brand. In 2022, Duolingo opened “Duo's Taquería” in Pittsburgh – a Mexican restaurant right next to its headquarters. This attracted worldwide press coverage (including the New York Times and Food & Wine) and turned the owl into a lifestyle icon. Revenue? Negligible at around $1.3 million in 2024, but priceless as a PR coup.

It's really shocking how little money Duolingo invests in traditional marketing. Growth is mainly driven by organic social media reach and word of mouth. Paid marketing is only used in a targeted manner – for example, in emerging markets or as small performance campaigns. Luis von Ahn put it this way:

“(...) we are not a company that puts out a product and then puts $50 million of marketing behind this product to make it grow from one day to the next. Our belief is that really good products should grow by themselves mostly. So we are going to put this out, but I would not expect that next year, for example, our math app suddenly has 50 million users and make $50 million of revenue.” – Luis von Ahn, Q3-2021 Earnings Call

Interim conclusion on branding 📣

The Duolingo brand is globally strong, creative, and highly emotionalized among younger target groups.

But unlike luxury brands, for example, this brand strength does not translate into pricing power. Subscription prices cannot be increased at will.

In markets such as India in particular, the management itself has emphasized that current price levels are already too high.

The strength of the branding therefore clearly lies in its reach, recognition, and viral effect. And less in margin increases through premium prices. This power can therefore be classified as weak.

VII. Process power thanks to a first-class culture ⚙️

Duolingo clearly demonstrates how to make learning fun while continuously improving it with a data-driven approach. As already mentioned, A/B testing, BirdBrain, and AI-generated content are the tools that optimize user experience, subscriber numbers, and monetization step by step.

“We experiment relentlessly to improve user experience and monetization. Through gamification, social features, and our social-first marketing, we scaled our reach, converted more free users into subscribers, improved learning outcomes, and maintained strong profitability.” – Luis von Ahn, Q4-2024 Earnings Call

On the surface, the app appears playful, almost like a simple mobile game. But there is much more to the green owl than meets the eye:

“(…) a surface-level look at Duolingo can be misleading because the app looks so cute and gamified that many people don't realize the amount of sophistication that is in the background and how much personalization there is in the learning experience.” – Luis von Ahn, Q3-2021 Earnings Call

To further improve the app, the company is working on 3 key pillars: monetization, engagement, and learning. Each of these pillars is handled by a similarly sized team, ensuring a balance between user retention, learning success, and revenue.

“The way we operate for the Duolingo app is (…) there's three main things we want to improve.

We want to monetize better.

We want to make it more engaging, and

we want to teach better.

(...) So we have about equal number of people working on each one of them.” – Luis von Ahn, Q3-2024 Earnings Call

The process power is also evident in its efficiency: Duolingo pursues a product-led growth model. As mentioned, traditional paid marketing is minimal; instead, reach and user growth are achieved through gamification and organic social media campaigns.

A particularly exciting example of this culture is the new chess course. It was initially developed by just two Duolingo employees—without any programming knowledge or chess experience. With the help of AI, a functional prototype was created, which was then professionalized by a larger team.

“I should mention something amazing about the chess is that it really started with a team of two people, neither of whom knew how to program, so they were not programmers.

And they basically made prototypes and did the whole curriculum of chess by just using AI. Also, neither of them knew how to play chess. And we started that for several months, and eventually, when they had a really good prototype, we had a a whole team to, you know, professionalize it and and put it in the app.” – Luis von Ahn, Q1-2025 Earnings Call

In my opinion, the chess course is a very good indication of the culture of experimentation at Duolingo. Innovations and new products can be developed and implemented in a decentralized manner.

In this podcast with Tim Ferriss, Luis von Ahn provides a few more insights into the corporate culture. He talks about how low the employee turnover rate is at Duolingo. The majority of employees have been with the company since it was founded in 2011.

However, I find this part of the podcast particularly interesting, where Luis describes the culture of constant optimization at Duolingo:

“In many companies, the normal thing to do is that you have a leaderboard team, a team that owns that big feature; so just kind of, you split it up by feature. These are feature-based teams. We do not do feature-based teams; we do metrics-based teams. So, we don't have a team that owns the leaderboard.

Instead, we have a bunch of teams that each own a single metric. For example, a metric that we have is time spent learning. What they own is the number of minutes per day that the average user uses Duolingo for. And it turns out that changes to the leaderboard increase—or can increase or decrease—time spent learning if you do kind of the right or the wrong thing.” – Luis von Ahn on The Tim Ferriss Show

Interim conclusion on process power ⚙️

Duolingo's process strength is based on excellent talent, decentralized team structures, and a very strong culture of experimentation.

The best example of this culture of experimentation is the new chess course: two Duolingo employees developed it single-handedly, but neither of them knew how to program or even knew the rules of chess.

As a result, Duolingo appears to be a playful app on the surface. In reality, however, the app is based on one of the most powerful learning platform infrastructures in the world.

Therefore, I rate Duolingo's process strength as strong.

5) Analysis of the financial situation

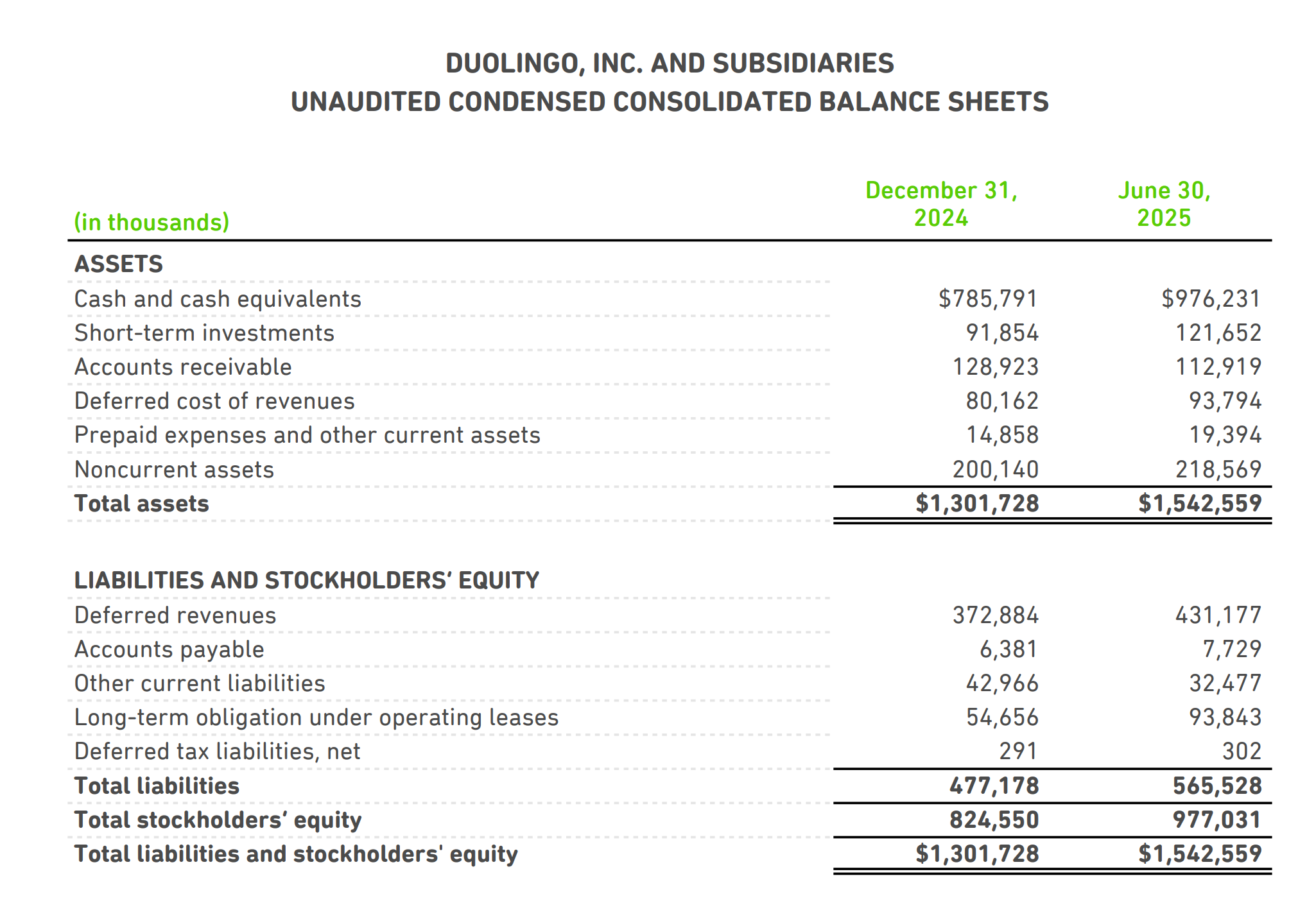

Duolingo's financial situation is truly excellent, as its balance sheet is very solid. At the end of Q2 2025, the company had approximately $1.1 billion in cash ($976 million in cash plus $121 million in short-term investments) and no debt whatsoever. In fact, the majority of the assets (71%) on the balance sheet consist solely of cash, which is very good.

On the equity and liabilities side, which represents the company's financing structure, the picture is similarly positive. Equity accounts for 63% of the balance sheet total (equity ratio). In addition, there is a special feature of the business model: deferred revenues.

This refers to advance payments from annual subscribers: they pay the entire amount at the beginning, but Duolingo is not allowed to record this as revenue immediately. Instead, the annual subscription amount is spread over the term of the subscription. The total amount is then gradually recorded as revenue month by month.

To make this more tangible, here is an example: With a Duolingo Max annual subscription ($167.99/year), the money goes straight into the coffers. However, for accounting purposes, the amount is initially recorded in full as “deferred revenue” on the liabilities side of the balance sheet. Each month, around $14.00 is then recorded as revenue until, after 12 months, the full amount is realized as revenue.

This deferred revenue amounted to $431.2 million (Q2-2025), which represents almost 28% of the total balance sheet. Equity plus deferred revenue together account for 91% of the balance sheet total. This underscores how strong and sustainable Duolingo's financing is. It is more than sufficient to finance the company's future growth.

6) Close-up look at the valuation of Duolingo shares

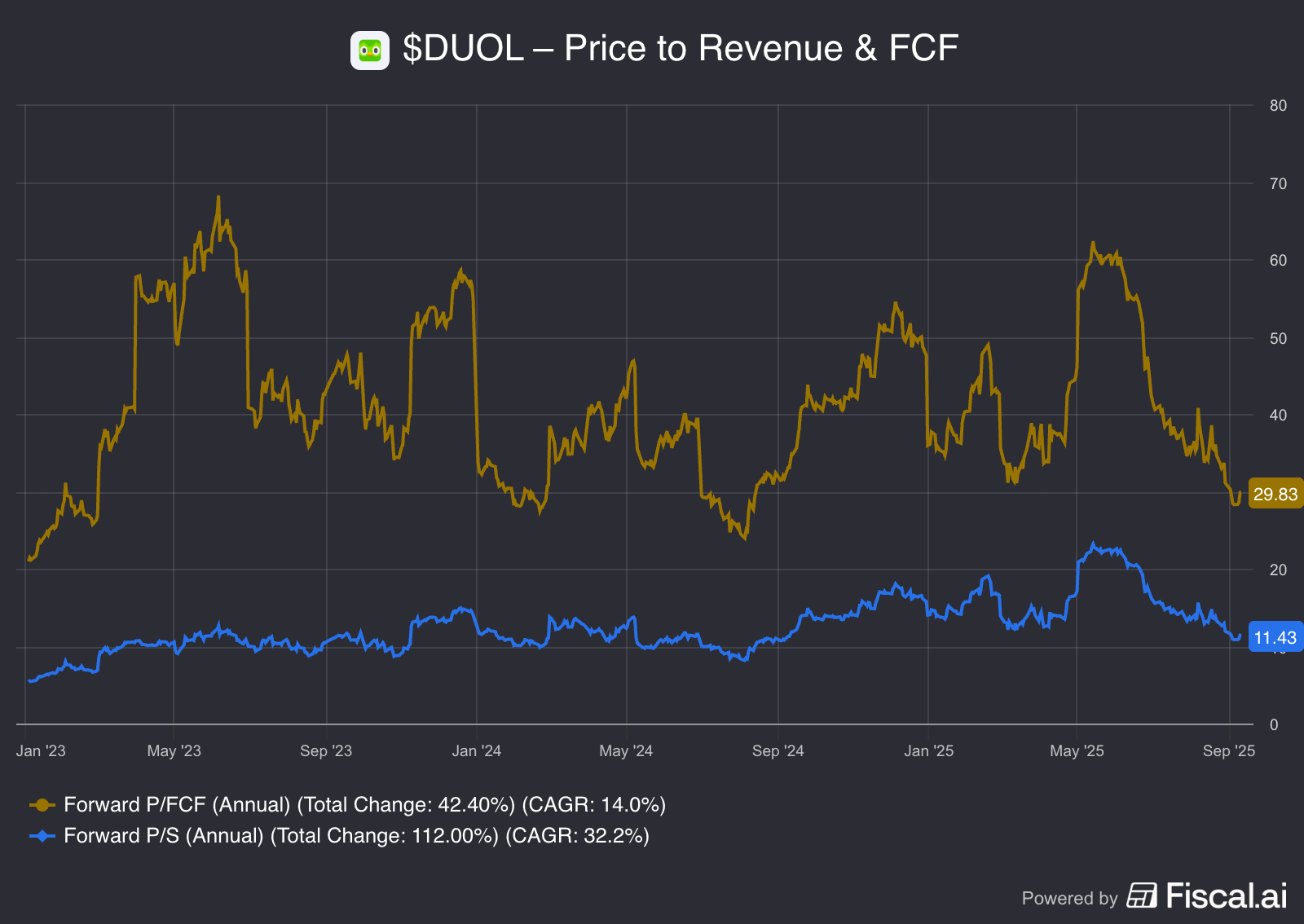

Duolingo is clearly a growth company and is not yet optimized for maximum profits. Nevertheless, the stock is trading at around 29.8 times free cash flow over the next 12 months. This puts the stock at the lower end of the range for the last three years. The high point here was 70.

A look at the valuation in relation to sales shows that the stock is in the middle range for the last three years: currently valued at 11 times revenue, but the range has been from a factor of 5 to 20.

Although this seems quite high, it is more than justified in the context of the excellent growth rates and profit margins.

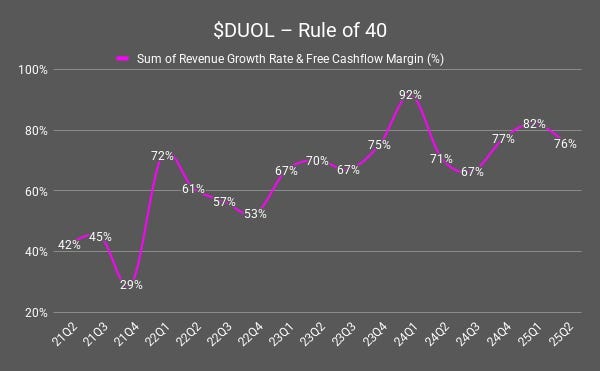

An important metric for assessing how profitably growth stocks are growing is the “Rule of 40.”

This is calculated by combining the revenue growth rate and profit margin.

If this figure is above 40, it is a very good sign.

In Q2 2025, this figure was a paranormal 76% for Duolingo (revenue growth of 42% plus free cash flow margin of 34%), almost twice as high as the eponymous 40. That is truly extraordinary.

7) Risks due to high valuation, expansion, and AI

In addition to its many positive aspects, Duolingo as a stock also has risks. As with other growth stocks, if Duolingo fails to meet its expected growth and profitability targets, its high valuation could quickly collapse.

Another important growth driver for Duolingo is the Chinese market. However, expansion there is proving more difficult than expected. One key reason is that the AI tutor Lily is based on OpenAI technology (ChatGPT). Since OpenAI products are completely banned in China, Duolingo is currently unable to offer its service there as usual. The company is working on implementing a locally approved AI solution, but this is a complex and lengthy process. This challenge is critical because China is one of the fastest-growing markets (Q2 2025).

“At the moment, we have really put Duolingo Max in mostly every country. There's a couple of countries where it's not at. For example, it's not in China simply because we cannot serve things from OpenAI in China. So, we're going to have it there, but it's not there yet.” – Luis von Ahn, Q4-2024 Earnings Call

One risk frequently cited by critics is the potential disruption caused by generative AI offerings such as ChatGPT or Google Translator. However, these companies do not have Duolingo's extensive, specific language learning data, which is unique with over 50 million daily active users and precisely tailored to language learning processes. This proprietary database gives Duolingo a unique competitive advantage, as I explained earlier under Exclusive Resources.

Another potential threat to Duolingo is the new Apple AirPods, which will feature a real-time translation function. Starting in 2025, a firmware update will enable conversations to be translated live directly in the earbuds, facilitating communication between speakers of different languages.

Nevertheless, I consider the risk of Duolingo becoming redundant to be low. Although Apple AirPods can provide translations, they are more likely to promote intercultural exchange and thus interest in actually learning a language. Lowering barriers to communication can even increase actual language learning with Duolingo. It's like a kind of Jevons paradox, where easier access to languages increases the need to learn.

8) My conclusion

Duolingo is increasingly becoming a platform that enables personalized education for the mass market. This is something that has never been seen before in human history. The company is just getting started and aims to redefine the global education market.

In doing so, Duolingo will massively increase its revenue momentum and profitability in the coming years. The market still completely underestimates the qualitative changes in strategy and processes that have already been implemented. These will only become quantitatively visible in the figures step by step.

My investment thesis is based on 4 pillars: (1) The increase in the number of subscribers through viral marketing, combined with (2) higher revenue per subscriber thanks to the platform's increasing added value, will fuel the company's revenue growth for many years to come. In addition, (3) an improving cost structure, particularly due to falling AI costs for AI tutor Lily and more and faster content generation through AI. This should (4) massively increase free cash flow per share and, as a result, also drive Duolingo's share price in the long term.

The foundation for these extraordinary developments are the competitive advantages that give the company economic benefits and protect it from competitors. I see Duolingo's strong competitive advantages as being its exclusive resources thanks to its huge data treasure trove and AI integration, economies of scale with falling unit costs, and process strength, which is reflected in a consistent culture of experimentation and data-driven optimizations. The network effects are solidly established thanks to the growing database, which improves the learning experience for everyone, and the switching costs due to subscription loyalty, personalization, and gamification features such as streaks. The overall picture is rounded off by the branding, which generates enormous reach and viral marketing but does not offer any real pricing power.

However, there are also risks. Duolingo is clearly classified as a growth stock and is therefore susceptible to valuation risks. If the company fails to meet its expected growth or profitability targets, the share price could quickly fall sharply. Expansion in China is also critical, as OpenAI products are banned there and Duolingo needs a local solution for its AI tutor Lily. Advances in technologies such as generative AI or live translation via Apple AirPods are also often cited as risks. In my view, however, they tend to increase interest in language learning, while Duolingo's unique learning data continues to secure a clear advantage.

According to my analysis, the risk-reward ratio for Duolingo remains clearly asymmetrical: manageable risk and high potential. The current discount of more than 40% to its all-time high is attractive. This means that the stock is trading at 30 times the expected free cash flow (FCF) for the next 12 months and has increased FCF by over 50% in the last quarter (FCF per share LTM in Q2-2025).

This led me to build up an initial position in Duolingo. After all, the company shows many characteristics of a potential tenbagger over the next 5-10 years. I plan to make further purchases and hope that the stock will continue to fall so that I can buy more at a lower price.

Disclaimer: I have prepared this analysis to the best of my knowledge and belief. It is for information purposes only and does not constitute investment advice or a recommendation. I do not guarantee the accuracy, completeness or timeliness of the data contained herein.

👉 Follow me now on X at @aktien_max for more analysis.

$TSLA is creating the infrastructure for AI in the real world (outside the cloud)

FYI: This is the English translation of my Deep Dive in German. For the German version, please click here.