How $HIMS is reshaping the US healthcare system....

Deep Dive - English Edition

FYI: This is the English translation of my Deep Dive in German. For the German version, please click here.

Hims & Hers, Inc. (ticker symbol: $HIMS) is an exceptional company that, in my analysis, has an asymmetric risk/reward ratio - and not just because the stock is 30% below its all-time high.

With a market capitalization of $12 billion and a valuation at 5x expected 2025 revenue, the stock market is completely ignoring the special characteristics of this company.

In my view, this could be because many analysts are overly focused on one area of Hims' business and are overlooking the rest of the company and missing the bigger picture - but more on that later.

Hims' exceptional attributes can be seen in the development of the following 4 metrics:

Growth in the number of subscribers

Increase in revenue per subscriber

Optimization of the cost structure

Development of free cash flow per share

The stock is about to reach a tipping point

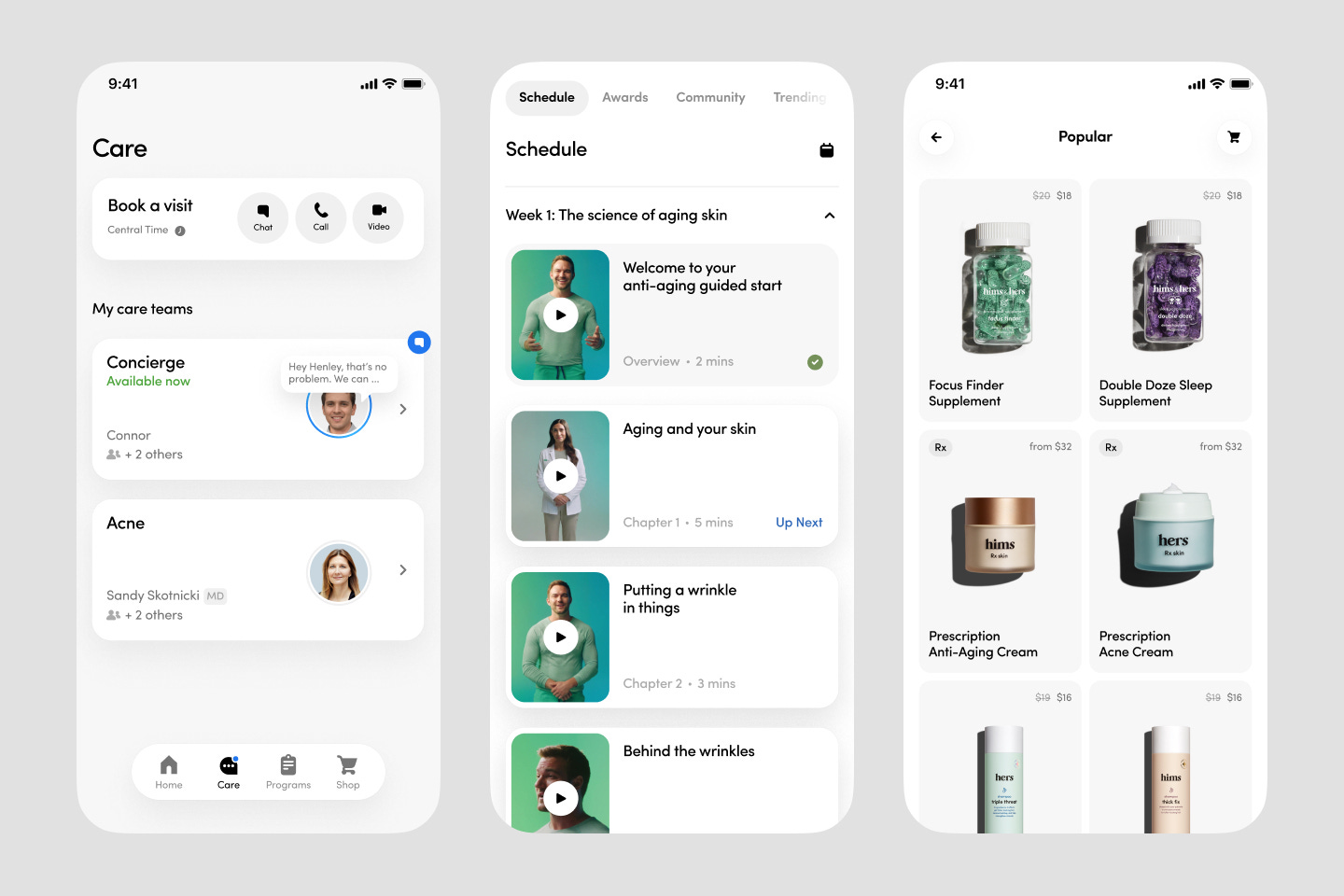

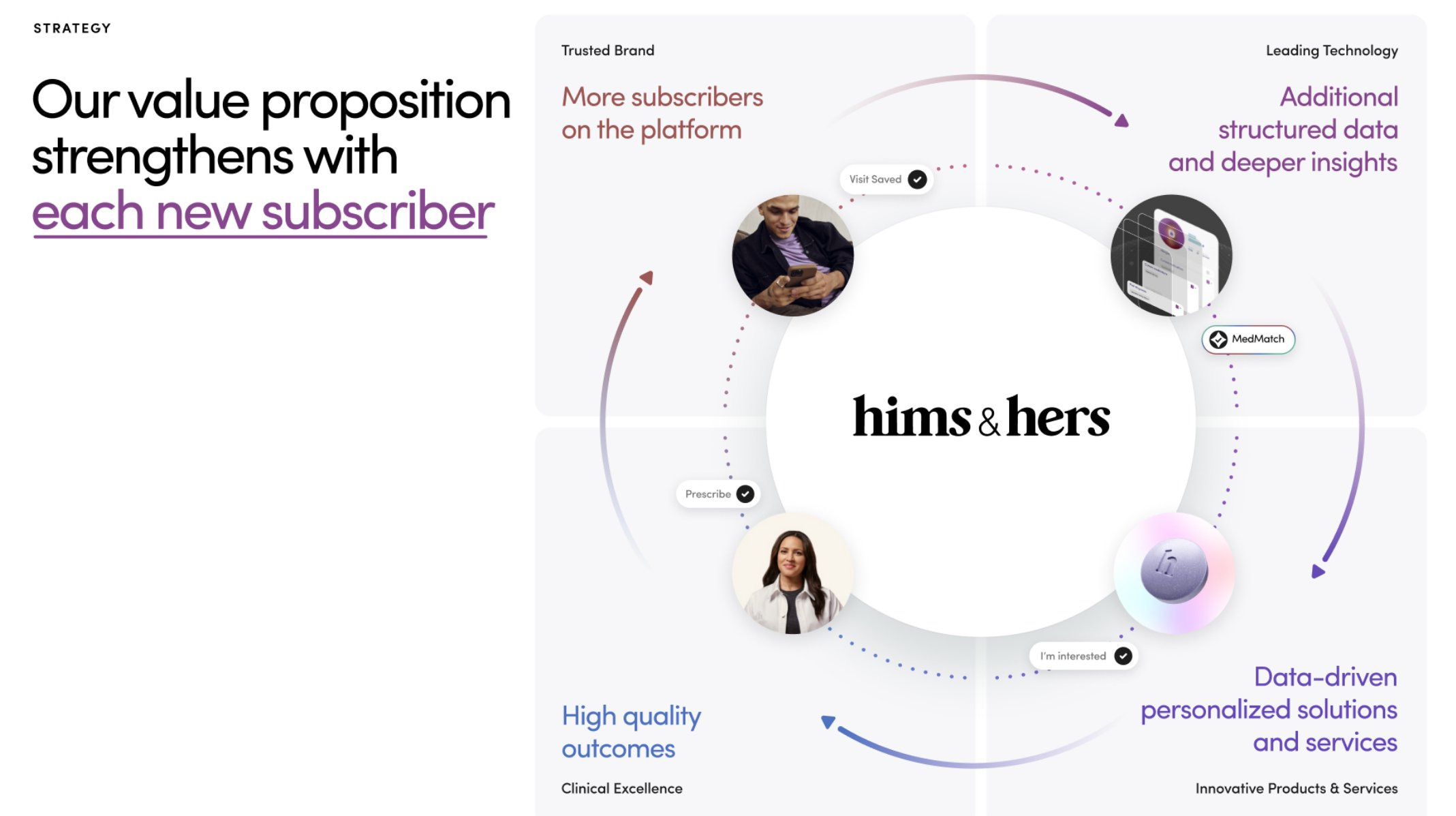

Although Hims may look like just another telemedicine provider at first glance, there is much more to it than that. Hims is building a universal healthcare platform that covers the entire healthcare process - from consultation and diagnosis to treatment - all from a single source.

The Hims process generally works in 5 steps:

Registration & questionnaire via app or website

You create an account in the Hims app or on the website, select your health topic (e.g. hair loss or skin problems) and answer a few personal questions about your medical history and symptoms.

Tele-doctor consultation & prescription

A Hims doctor looks at your answers and gets in touch via video chat or phone to clarify any unanswered questions. If everything checks out, you'll receive an electronic prescription straight away.

Select product & pay

As soon as your prescription has been approved, you select the exact medication and pack size you need. You enter your shipping address and pay - you can also set up a subscription so that you automatically receive your medication at regular intervals.

Discreet packaging & shipping

The Hims pharmacy prepares your medication, packages it discreetly and sends it directly to your home. You will receive a tracking number so that you can track when it arrives at any time.

Further support & subscription service

If you have any questions or notice a change, you can speak to the Hims team at any time by chat or phone. Your subscription continues automatically - and if you want to take a break or adjust something, you can do so at any time.

Now it gets more interesting: In the process, the company is using data-driven feedback loops to offer personalized and cost-effective healthcare solutions - something the inflationary US healthcare system does not know.

The company is therefore about to reach a tipping point that will take revenues to a new level and significantly increase profitability.

These metrics show the progress

If you look at these 3 metrics, you will see that the speed at which Hims can move into new areas and scale them is increasing rapidly. In addition, the level of personalized treatments they offer is also increasing.

These are the 3 KPIs that we will now analyze in more detail:

Growth in the number of subscribers

Development of revenue per subscriber

Optimization of the cost structure

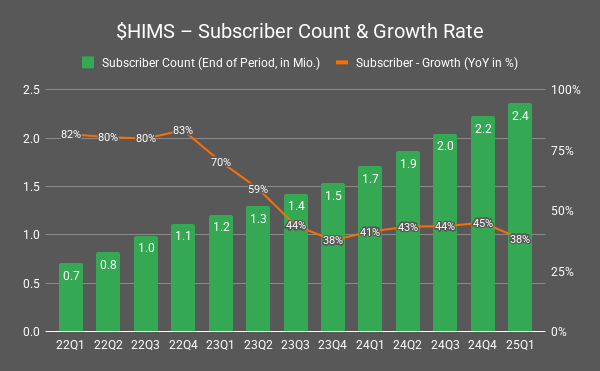

Strong growth in the number of subscribers

Since Q1-2022, the number of subscribers on Hims platform has increased from 710,000 to over 2.4 million (Q1-2025) - a total of 238% or 50% growth per year. This trend is driven by a clear marketing message and cost-effective offers for the treatment of many stigmatized conditions - including hair loss, erectile dysfunction, skin problems and obesity.

In my view, Hims is still at the very beginning of its journey with around 2.4 million subscribers (Q1-2025). In the USA alone, Hims has a potential target group of over 80 million people in each of its relevant areas - so the market is huge and offers plenty of room for growth in the long term.

Breakout in revenue per subscriber

The average revenue per Hims subscriber has been moving sideways for a long time. I use the term average revenue per user (ARPU) synonymously here because this is a key figure for many software and ad-financed business models in the tech industry - I also consider Hims to be a tech company, and therefore refer to this key figure in a similar way.

Starting around Q1-2022, the average revenue per subscriber (based on the last 12 months, LTM) gradually increased from $559 to $844 in Q1-2025. This results in a growth of 50% or 15% per year, driven by (1) more treatments sold per subscriber, (2) higher-priced treatments in the product mix and (3) a greater degree of personalization of the services offered.

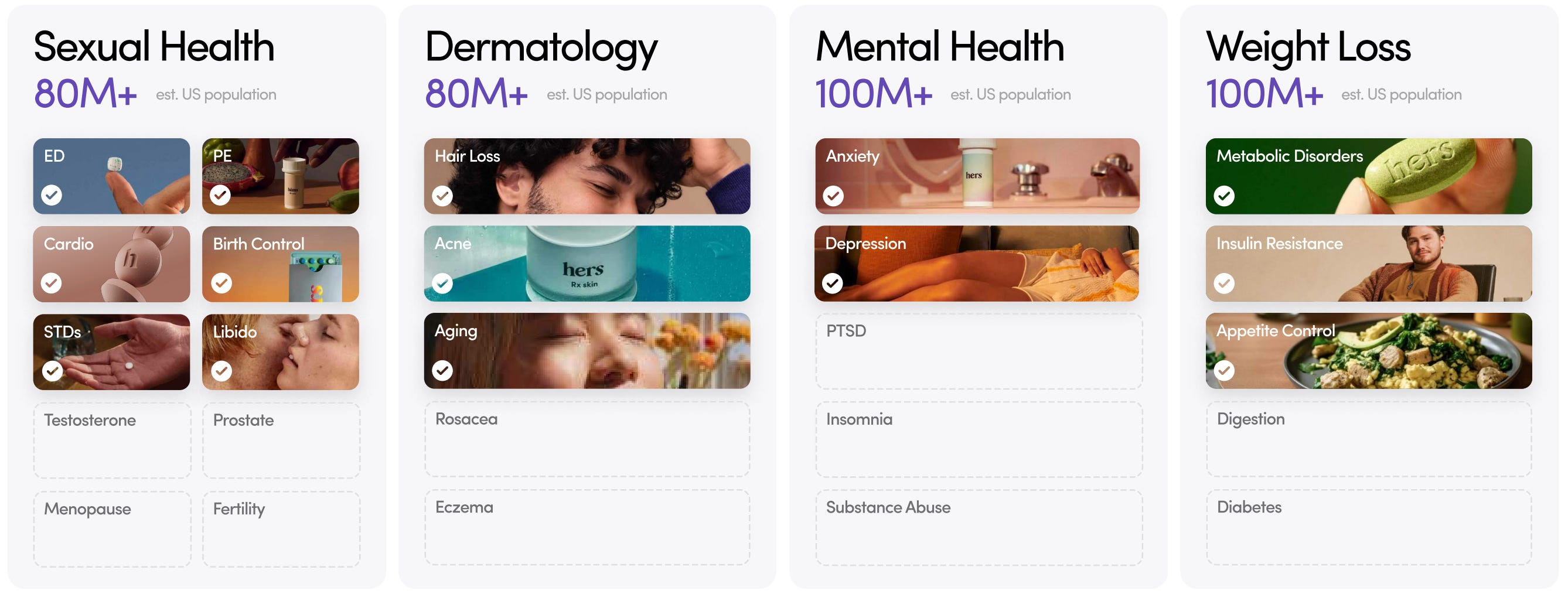

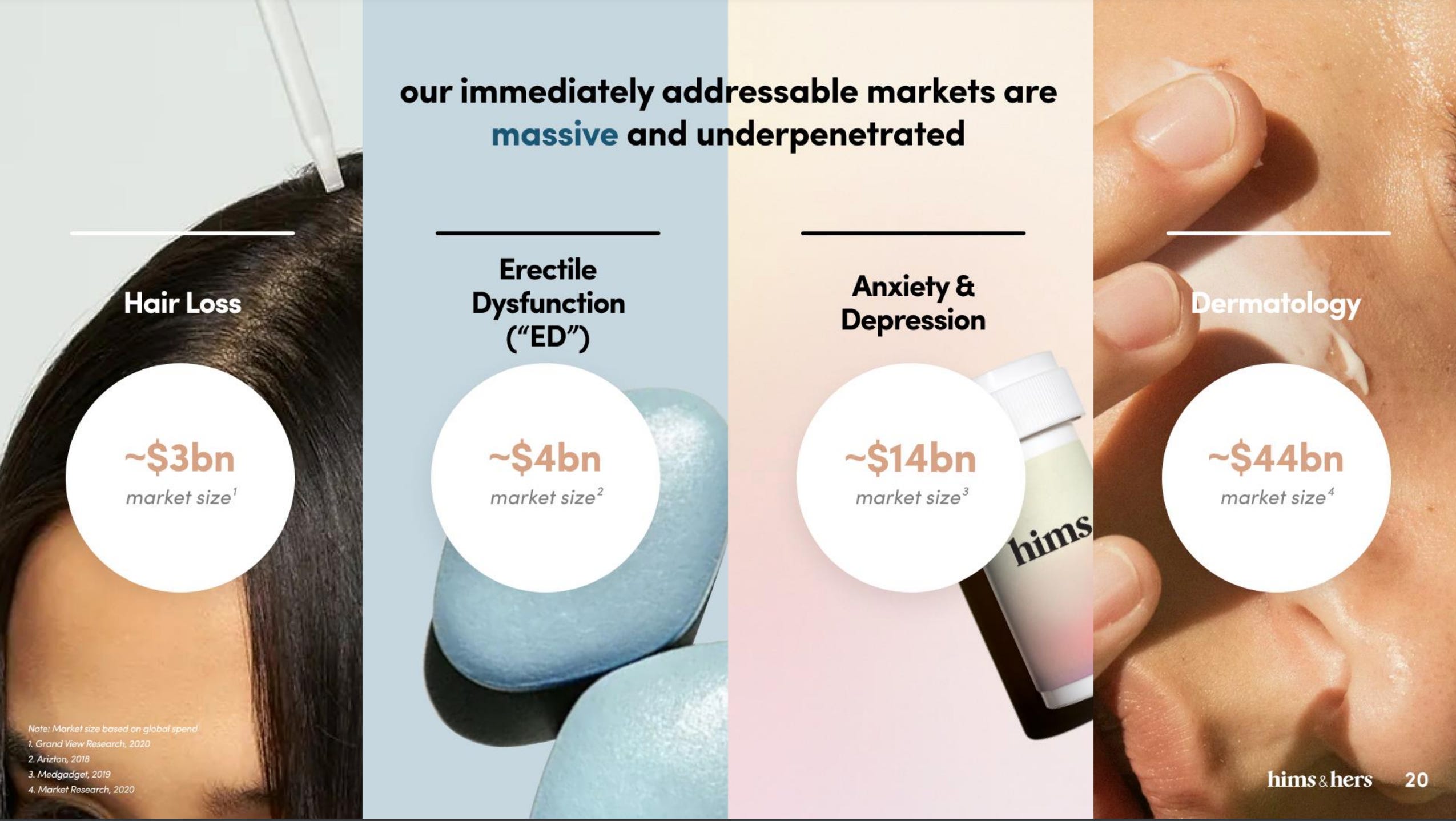

In my view, Hims is still in the early stages, as the company is only active in 4 areas of the global healthcare market, which have a combined market volume of $65 billion (Hims sales 2024: $1.5 billion):

Hair loss: $3 billion

Erectile dysfunction: $4 billion

Anxiety & depression: $14 billion

Dermatology: $44 billion

I therefore assume that Hims will increase its revenue per subscriber many times over in the long term. The US healthcare market alone has a market volume of almost $5 trillion - that's $5,000 billion!

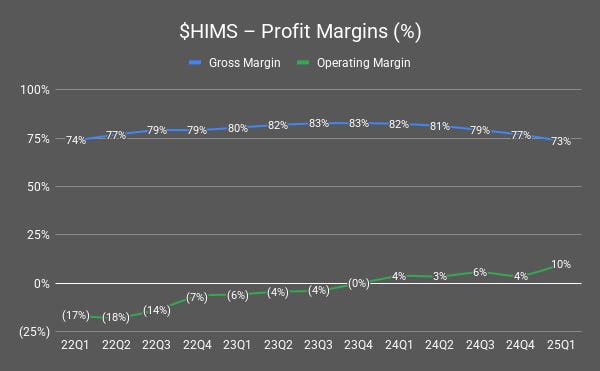

Optimizing the cost structure

In addition to increasing subscriber numbers and more revenue per subscriber, Hims is constantly improving its cost structure.

Let's start with the company's margin,s which are already very high: In the last 3 years the gross margin was between 73% to 83%. This is because only the direct costs (for generic drugs, packaging, shipping and salaries for doctors and pharmacy staff) are included in the cost of sales. Everything that is not directly related to the manufacture or delivery of products (marketing, administration, research and development) is included in operating expenses (OPEX). As a result, the gross margin is correspondingly high.

However, Hims has also been able to improve its operating profit margin (gross margin less operating expenses) over the last 3 years. The operating margin has climbed from -17% (Q1-2022) to 10% (Q1-2025) because Hims is constantly achieving better economies of scale and efficiencies in its supply chain.

A relevant trend in this context is the ratio of operating expenses (OPEX) to revenue. It is clear to see that OPEX has fallen from 90% of sales (Q1-2022) to 64% of sales (Q1-2025) - a huge improvement in just 3 years!

The drivers behind this are the trend of the 4 categories that add up to OPEX:

🔵 General & Administrative

General and administrative costs ranged between 8% and 22% of revenue (Q1-2022 to Q1-2025) and are currently at 8% (Q1-2025).

These are all costs that are necessary for the company to function smoothly internally (e.g. accounting, management, HR), and the decline shows that Hims has become more efficient in this area.

🟨 Tech & Development

Spending on technology & development was between 5% and 6% of revenue and is currently 5% (Q1-2025).

In this way, Hims ensures that the digital platform, apps and new products are constantly improving. In my opinion, Hims has achieved a good balance between innovation and cost control.

🟥 Operations & Support

Operating and support costs ranged from 11% to 15% of revenue (Q1-2022 to Q1-2025) and are currently 11% (Q1-2025).

This includes all costs for logistics, warehousing, customer service and quality assurance. The decline shows that supply chains and service processes are now leaner and more cost-efficient.

🟩 Marketing

Marketing expenses fluctuated between 39% and 54% of revenue (Q1-2022 to Q1-2025) and have currently fallen to 39% (Q1-2025).

As expected, Marketing is of course the key growth driver at Hims to attract more customers through advertising and brand building. The decrease compared to revenue means that Hims is now using more organic reach and more efficient campaigns to attract new subscribers. Management expects to save around 1-3% percentage points per year in the ratio of marketing spend to revenue. If this works, the profit margin should increase significantly over the next few years.

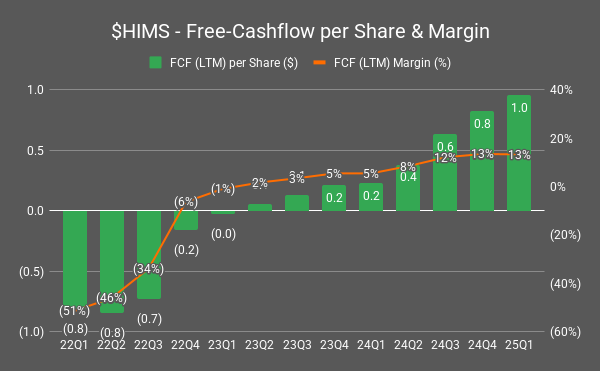

Rising free cash flow as a result

In my view, the revaluation of Hims shares will occur when the strong fundamental development of the various business areas (hair loss, sexual health, skin problems, weight loss, etc.) and the improved cost structure become increasingly visible in the financial metrics and the stock market notices this.

The important KPI in this context is the free cash flow (FCF) per share (in the last 12 months, LTM), which has exploded from -$0.82 in Q1-2022 to $0.96 in Q1-2025. Year-on-year alone, FCF has shot up by over 320%, more than quadrupling.

In the same period, the free cash flow as a percentage of sales (FCF margin) more than doubled from 5.4% to 13.3%. I expect these positive developments to continue as more of Hims' businesses progress in development, scale and level of personalization.

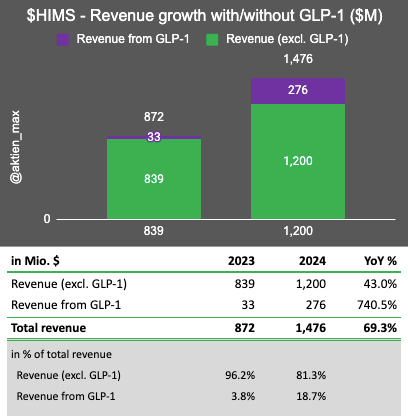

However, as mentioned earlier, the stock market is still quite focused on Hims' weight loss segment, which will account for about 30% of sales in 2025 - as Hims' 2025 guidance calls for $2.4 billion in total sales, $725 million of which will come from weight loss drugs.

The stock market is particularly concerned about weight loss drugs with the GLP-1 active ingredient, which makes up part of the weight loss segment. This is because much of the rapid sales growth of 69% in 2024 came from the provision of semaglutide under FDA emergency clauses.

Specifically, revenue with GLP-1 grew by an insane 740%, while revenue without GLP-1 “only” increased by 43% in 2024. Without this driver, many analysts consider the future scaling of the sales segment to be questionable. Some stock market participants even fear declining sales.

At the beginning of 2025, the US Food and Drug Administration (FDA) withdrew the exemption approval for the low-cost compounding of semaglutide in Him's own pharmacies. Compounding refers to the production of individual formulations in pharmacies, in which active ingredients are processed into customized medications. Hims had been processing semaglutide in its pharmacies - the same active ingredient that Novo Nordisk uses in its patented weight loss drugs Wegovy and Ozempic.

As a result of the loss of the exemption approval, Hims must therefore switch from high-margin compounds back to more expensive branded preparations, which mean lower profit margins for the company - at least that is what the stock market fears. Nevertheless, Hims will continue to mix Semaglutide itself if it is really medically necessary, for example in the case of an allergy to an ingredient of the original product.

Of course, there are still legal and regulatory uncertainties because both Novo Nordisk and Eli Lilly are suing copycat GLP-1 suppliers. However, Hims has been able to address many of these concerns through its partnership with Danish pharmaceutical giant Novo Nordisk since April 2025. A clever move that, in my view, demonstrates the company's special organizational characteristics, which I will explain in the next section.

Strong company culture leads to growing moat

Despite its short existence - the company was founded in 2017 - Hims has managed to establish a strong mission that not only attracts but also retains top talent. In my view, this is probably the most important input in building an exceptional company.

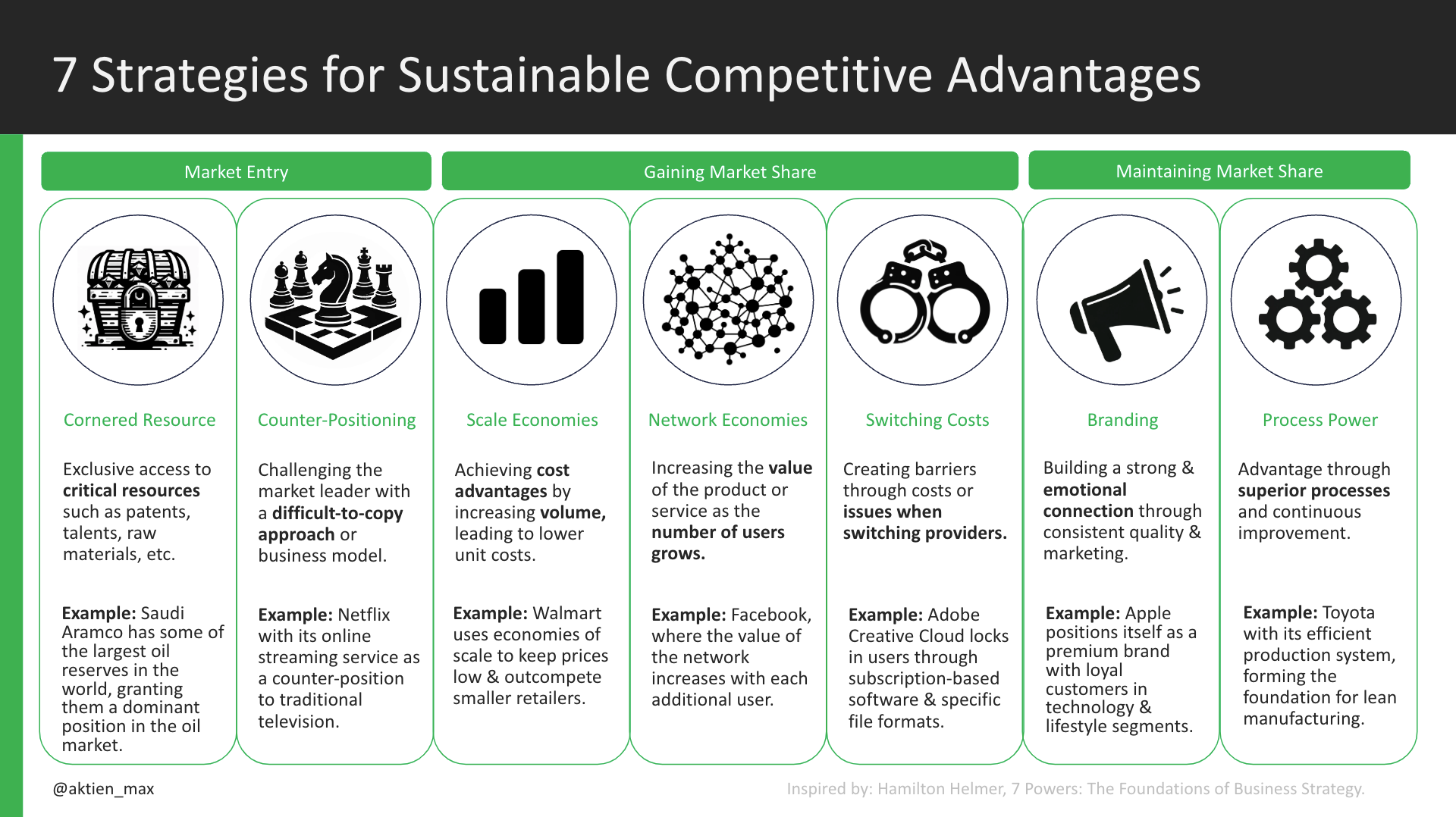

At Hims, teams work together in systems that deliver results at incredible speed and quality. This has led to the following 7 competitive advantages that are almost impossible to replicate in total - even Amazon has failed to do so:

Cornered resource 💎

Counter-positioning ⚔️

Scale Economies 📈

Network effects 🔄

Switching costs 🔗

Branding 📣

Process power ⚙️

Let's look at these 7 moats in more detail:

Cornered resource through data treasure 💎

At Hims, I consider access to proprietary patient data from its approximately 2.5 million subscribers (Q1-2025) to be an cornered resource. Cornered resource means that a company has exclusive control over a valuable resource that cannot be easily copied or replicated by competitors. Classic examples of this are valuable raw material deposits or patented drugs.

By acquiring the at-home lab testing facility Sigmund NJ LLC (known under the brand “Trybe Labs”) on February 19, 2025, Hims has taken an important step in this direction.

Hims intends to expand its offering to include at-home blood testing and comprehensive whole-body testing. But how exactly does it work?

With Trybe Labs, you simply prick your fingertip with a small lancet at home and receive everything you need via a blood test - from hormone and cholesterol levels, liver and thyroid function to heart, stress and prostate checks.

The raw data obtained in this way is used both for personalized treatment planning by the telemedicine providers and anonymously in the further development of AI tools (e.g. MedMatch) to make treatment recommendations even more precise.

This enables Hims to better assess its customers and offer suitable treatments, which should drive revenue per subscriber.

In the long term, the at-home test offering should enable Hims to expand new clinical categories such as low testosterone and menopause support more quickly and to tap into other specialty areas (longevity, preventive medicine, etc.) through data-driven insights.

I consider this competitive advantage to be weak - it is still in the early stages, but the course has been set in the right direction.

Counter-positioning through VIMPRO approach ⚔️

Hims is pursuing a strategy that clearly differentiates the company from both traditional healthcare providers and competitors such as Teladoc ($TDOC). I see this as counter-positioning - this means that a company deliberately positions itself differently from established competitors in order to exploit their weaknesses and thus stand out in the market. This is because the established players are often afraid of damaging their core business and are reluctant to switch to the new approach.

While traditional providers rely on physical pharmacies and doctors' surgeries, Hims offers a fully digital experience where medication is delivered directly to customers' doorsteps. This is particularly beneficial in sensitive and stigmatized areas such as sexual health and hair loss, as it offers customers discretion and convenience. Who wants to go into a pharmacy and ask what helps with erectile dysfunction?

Hims is also pursuing a different business model here: the company sells directly to the self-paying end customer (D2C), while Teladoc operates primarily through employers and the US healthcare system, where companies pay for their employees' healthcare (B2B) - which unfortunately often means higher and increasing costs for the patient due to the poor incentives in the traditional US healthcare system.

The value chain at Hims is also structured differently, with the company distinguishing itself as a "Vertically Integrated Micro-Provider" (VIMPRO). This is in contrast to Teladoc, which primarily operates as a telemedicine platform and has basically outsourced the dispensing of medication to third-party providers. Hims, on the other hand, offers everything from a single source. This means that Hims customers not only receive medical advice, but also have the appropriate medication sent directly from the same provider.

This seamless integration of services enables Hims to make the entire process more efficient and customer-friendly. This type of counter-positioning is difficult for competitors to imitate, as they often rely on external partners and do not have the same control over the entire process. I consider this competitive advantage to be already well developed at Hims.

Scale economies through growing size 📈

Hims also benefits from economies of scale, which enable the company to reduce costs and offer competitive prices at the same time.

By selling large quantities of standardized health products (hair growth products, skin care products, etc.), Hims can achieve better cost structures in purchasing and manufacturing. To this end, Hims operates an FDA-registered 503A pharmacy facility (i.e. a compounding pharmacy) in Ohio and Arizona, where individual formulations (e.g. topical hair and skin preparations) are produced. In California, Hims has a peptide production facility (a specialized laboratory facility) where active ingredients for its own preparations are developed and produced.

Another decisive factor in the economies of scale is the operation of its own warehouses. These enable Hims to manage the entire supply chain efficiently and optimize logistics costs. As Hims can spread the fixed costs of the logistics infrastructure over a larger number of units of medicines sold, cost efficiency is further increased.

Because Hims has more control over its value chain, the company has also been able to achieve better cost structures than its competitors. Hims has also passed this on to its customers through lower prices - with the result that more customers come to Hims and stay there

This principle is called “Scale Economies Shared”:

When unit costs fall, the company passes the savings on to customers in the form of lower prices.

This increases demand, which in turn leads to even higher quantities and further decreasing costs - a self-reinforcing cycle.

Hims has copied this approach from companies such as Costco, Amazon and Tesla, which also use the principle.

This can be seen in the proportion of revenue generated in the D2C telehealth market via Hims. Since 2020, Hims' market share has gradually increased from 10.1% to 47.5% in 2024, while other providers such as BetterHelp (Teladoc) & Co. have either stagnated or lost market share to Hims.

In my view, one reason for this gain in market share is Him's combination of scalable purchasing, production and optimized logistics, which gives the company a significant advantage over smaller competitors.

The smaller the competitor, the lower the sales volume and the higher the costs (and prices) per unit. In the long term, I assume that only a handful of providers will be able to establish themselves in the D2C telehealth market. This is because the battle for customers is brutal and the hurdles to sustainable profitability are high.

Hims has shown that at least 1.5 million subscribers are needed to operate the business model profitably - the majority of competitors do not have this size and are therefore losing money.

As Hims largely controls its value chain and customer experience as VIMPRO, the company can leverage stronger economies of scale than its competitors. Thanks to its more than 2.5 million customers (Q1-2025), I see the economies of scale as already solidly developed - and rising.

Network effects through data-driven individualization 🔄

For Hims, I see a clear path how the company can build strong network effects in the long term. As you probably know, positive network effects arise when a product or platform becomes more attractive as the number of users increases - either through direct connections between users (direct network effects) or by improving the offering through complementary factors (indirect network effects).

As already mentioned in the Cornered Resources section, Hims has access to an increasing amount of relevant patient data. This data is collected regularly and centralized and anonymized in a database.

Hims thus creates the ideal conditions for a proprietary database to which the competition has no or only very limited access. Hims calls this “MedMatch” and uses anonymized patient data to train AI models. The result: thanks to the individual patient data, patterns can be recognized that help in the prevention and treatment of diseases. With each new patient, the treatment and user experience of all users on the platform improves - a self-reinforcing feedback loop is set in motion.

In the Q4-2024 earnings call, Hims founder and CEO Andrew Dudum even said that in the long term, every patient will have a kind of “AI Health & Fitness Trainer”:

“One of the things that I think about a lot as an entrepreneur is what are things that the ultra-rich have access to? And then how can we broaden that and give that to everybody? So things that people have are on-demand therapists, right? They've got nutritionalists. They have fitness coaches. They have meditation coaches. These are people that are in your life, helping you to live healthier lifestyle. I think we are capable of building incredible AI versions of all of those coaches, which really changed the paradigm for how easy it is to change the lifestyle dynamics in your house and ultimately expand that to tens of millions of more people down the line. Now at the end of all of this, I think what is maybe even the most exciting from an AI standpoint is as we build these fairly proprietary models internally and validate them internally across our data set, (…)”

I still see the network effects at Hims in the early stages, but there is a clear way to see how the company can collect data that improves patient treatment in a meaningful way - personalized and at-scale.

Switching costs through increasing personalization 🔗

Another thing that should not be overlooked: Hims is increasingly building up switching costs through personalized offers, bundling and innovations that promote customer loyalty. On the one hand, this is achieved through customized solutions (like e.g. other dosages) that are tailored to the individual needs of customers. Secondly, through combination treatments that address several health problems at the same time.

These “one stop shop” offers make it unattractive to switch to another provider. Why take 5 tablets when you only need to take 1 tablet that covers all 5 things?

This is also the thinking of Hims' customers who use the company's personalized offers. This share of customers is growing disproportionately fast - in Q1-2025, almost 60% of Hims customers have already taken advantage of personalized offers - the 136% growth is about 3 times higher than the 38% growth in the total number of subscribers (Q1-2025).

By continuously introducing new products and formats, Hims ensures greater loyalty to the platform and the proportion of personalized products continues to increase. Regular innovations also improve the treatment experience and reduce customer churn.

However, I see the switching costs at Hims as slightly developed at the moment because the company has not been relying on such personalized offers for too long. It remains to be seen how well this will be accepted by customers in the long term and whether or not it will actually significantly reduce the churn rate among customers. So far, the developments look positive.

Branding through discretion, simplicity & trust 📣

A strong brand can become a competitive advantage. However, it is not just about awareness. A competitive advantage is only created when customers are willing to pay more for an objectively comparable product. This is achieved when the brand conveys a higher value from the subjective customer perspective. Then a company has achieved true pricing power.

Hims has already successfully managed to establish itself as a trusted provider of modern health solutions. Initially, Hims has pioneered a positioning in the niche for stigmatized health issues such as hair loss, skin problems and erectile dysfunction. In doing so, Hims is making a significant contribution to treating such conditions by offering treatments discreetly via their online platforms.

This allows people to seek help from the comfort of their own home and use the medication they need without feeling ashamed. Hims thus appeals particularly to younger generations who are looking for discreet and convenient solutions to their healthcare needs.

The brands “Hims” (for men) and “Hers” (for women) stand for accessibility, simplicity and discretion, which is particularly important in areas such as sexual health and hair loss. In my view, this positive brand perception leads to a high level of customer loyalty and ensures that customers return to the services of Hims & Hers again and again - on a monthly subscription basis.

This extends from Him's digital platform to the packaging of the products. Some will probably dismiss this as superficial, but packaging makes a difference to the customer experience - as Apple has already proven. What's more, with Hims, medicines for stigmatized conditions (such as erectile dysfunction or hair loss) usually come in unappealing boxes that almost say “You're sick!” Hims has turned this negative image on its head, because the Hims packaging looks more like that of beauty or lifestyle products.

Health and medication are both issues that are about trust. Trust that you have the right provider and the right treatment. With its brand, Hims has managed to scale to over 2.5 million subscribers and $1.5 billion in revenue since its inception in 2017 - very impressive. I don't see Hims having pricing power yet, but I do see broad brand awareness and a high level of trust. However, I am excited to see how Hims can further develop its brand in the future.

Process strength thanks to first-class talent ⚙️

Hims has built up process strength over time by optimizing its internal processes. Process strength refers to business processes that give a company a clear competitive advantage through exceptional efficiency, speed and quality and cannot be easily copied. It is therefore the DNA of the company that has been built up over years and decades.

It starts with the company's mission, which attracts many top talents: “Helping the world feel great through the power of better health.”

Once in place, employees work together in teams that are measured heavily on metrics such as subscriber retention, time-to-doctor and net promoter score (NPS). This is a rarity in the healthcare industry, as it is more a part of the corporate culture of many classic consumer apps such as Uber or Duolingo. However, Hims also takes this data-driven approach, which improves the customer experience.

The high degree of vertical integration at Hims is particularly crucial - because, as already mentioned, the entire value chain from the doctor's consultation to the dispatch of personalized medication and feedback loops is mapped with data. This requires a real range of top talent and these different disciplines have to work together successfully to support the growing number of customers - so far with success: 91% of employees say Hims is a great place to work.

Hims employs, among others:

Doctors and pharmacists for telemedicine and personalized prescriptions,

software developers and data scientists for algorithms and A/B testing,

product managers as well as UX/UI designers and behavioral scientists for the user experience,

Logistics and fulfillment experts for shipping and inventory management,

Regulatory and medical legal teams for compliance,

marketing and content specialists for brand development and

customer service employees for 24/7 patient care.

This was the only way the company could solve the many challenges in practice. For example, setting up efficient logistics and distribution systems that make it possible to deliver products to customers quickly and reliably - even with personalized medicines in sometimes sterile environments, this is anything but easy.

In addition, the digital processes in customer service and medical advice are designed to be efficient for both the customer and Hims. Here, Hims focuses on personalized treatment recommendations and tailor-made solutions, which increases customer satisfaction. These efficient processes help to keep operating costs low and improve margins, allowing the company to remain competitive in a highly competitive market.

Hims wins where Amazon & Co. fail

And that's really not easy: the joint venture "Haven" between Amazon, Berkshire Hathaway and JPMorgan Chase was abandoned in 2021 because it encountered several major obstacles. Here is a brief overview:

The goal of Haven was to reduce healthcare costs for Amazon, Berkshire Hathaway and JPMorgan Chase employees and improve the quality of healthcare.

However, the US healthcare system is extremely complex and despite the resources of the three companies, it was difficult to overcome this hurdle.

The different interests of the partners also made it difficult to develop a common strategy.

Finally, the project met with resistance from existing players in the healthcare system who did not want any changes.

In the end, the decision was made to dissolve Haven and instead pursue their own projects within the respective companies - so far with moderate success, as Amazon in particular has not been able to establish itself successfully despite several attempts.

Hims, on the other hand, has successfully established itself in this extremely difficult market, which clearly speaks for a strong corporate culture with clear process strength. Next, let's take a look at the company's financial position.

Solid financial position despite start-up phase

Hims' financial position is very good, as evidenced by its solid balance sheet. This is not a given for a company that was only founded in 2017 and which I still classify in the startup category.

The company has over $320m in cash and no debt (Q1-2025). In addition, Hims has consistently reported positive free cash flow in every quarter since Q1-2023 - the business is already self-sustaining despite high growth rates.

However, the company placed a convertible bond in May 2025, which was originally set at a volume of $450m. Somewhat later, it was increased to $870m, bringing Hims' cash holdings to around $1.2bn. In my view, the terms are quite favorable for Hims: the company receives $870m with a term of 5 years to implement topics such as global expansion (organically and through acquisitions), AI data development, laboratory diagnostics and personalized medicine.

At the same time, Hims pays no interest for the first 5 years, which clearly conserves cash given market interest rates of around 4% per annum. A company like Hims would probably pay 8% interest (or more) due to the higher risk, saving the company around $70m in interest payments per year. But why do investors go along with this?

Compared to corporate bonds with typical market interest rates of 4% (or more), a convertible bond with a 0% interest coupon like Hims is only possible if investors can get something out of the built-in conversion right.

Investors have the right to exchange their convertible bond for shares in the company at a predetermined price of $70.67 per share. If the Hims share price is then higher, investors convert because they can obtain the shares more cheaply. However, if the share price is lower, investors simply keep their bond in cash until redemption.

Even in the event of a conversion, existing Hims shareholders would only be diluted by around 5%. This is because in Q1-2025 Hims had around 246m shares outstanding and the convertible bond would mean around 12m new shares - but only if the $70.67 per share is reached, which equates to around $18bn market capitalization. I consider the 5% additional dilution over 5 years to be reasonable.

Funds from convertible bond accelerate growth

I expect that the additional funds of almost $1bn that Hims has received thanks to the convertible bond will continue to drive growth.

This will bring the company faster towards the turning point I mentioned earlier: growing subscriber numbers and revenue per subscriber thanks to more treatment options (hair loss, sexual health, skin problems, weight loss, etc.) meets an improvement in the cost structure. This fundamental improvement is becoming increasingly visible in the financial figures - especially in the form of rising free cash flow per share - which the stock market should also notice.

Possible short squeeze due to rising short positions

The fact that over 27% of Hims shares are sold short is also important at this point. Hims is very popular with short sellers due to the GLP-1 uncertainties. But as soon as the company's progress leads to better financial figures, it could lead to a short squeeze.

As you probably know, a short squeeze happens on the stock market when many investors bet on falling prices - i.e. short a stock - and the price then suddenly rises sharply. It goes something like this:

Short sellers borrow a stock, sell it immediately and hope to buy it back later at a cheaper price.

If the price suddenly rises instead of falling, they come under pressure to close their position in order to limit losses.

To do this, they have to buy the share back - and this pushes the price up even further.

This sudden buying frenzy can cause the share price to explode, even though there are no fundamental reasons for this.

Because the short interest in Hims is relatively high at over 27%, the probability of a short squeeze increases significantly. At the beginning of 2025, the share price had already more than doubled within 6 weeks due to a short squeeze - this could happen again and short sellers could suffer heavy losses, real 4th degree burns. Let's see if they learn their lesson: never bet against an exceptional company.

My summary of Hims & Hers

Based on my analysis, the stock of Hims & Hers still shows an asymmetrical risk/reward ratio.

This is because Hims will significantly improve its profitability through (1) increasing subscriber numbers, (2) more revenue per subscriber and (3) a better cost structure. In this context, the development of the free cash flow per share is particularly important to me.

Hims is well on its way to becoming a universal healthcare platform that covers the entire healthcare process - from consultation to diagnosis to treatment - all from a single source. This will allow Hims to turn the inflationary US healthcare system around by offering lower prices and personalized products.

At the same time, the stock continues to trade at 5x expected 2025 revenue - around 30% below its all-time high.

In addition, over 27% of Hims shares are shorted and the stock market is critical of Hims' weighloss segment - but this is only one of several segments. However, as soon as Hims continues its strong fundamental development, the stock market will reward this. Even another short squeeze is possible in the short to medium term. In the long term, however, the share follows the free cash flow per share, which is like the force of gravity.

I first invested in Hims at the beginning of 2022 at prices of less than $5 per share and have built up my position over time.

Hims is still at an early stage and faces major hurdles. Nevertheless, the company has so far been able to handle many challenges very well thanks to its corporate culture - challenges that even much larger players such as Amazon, JPMorgan and Berkshire Hathaway have failed to overcome.

Due to these exceptional characteristics, I believe it is likely that Hims will become at least a tenbagger by 2030 - from the current share price level. In the long term, I see even more upside potential for the share.

I will continue to follow the development of Hims.

Disclaimer: I have prepared this analysis to the best of my knowledge and belief. It is for information purposes only and does not constitute investment advice or a recommendation. I do not guarantee the accuracy, completeness or timeliness of the data contained herein.

👉 Follow me now on X at @aktien_max for more analysis.